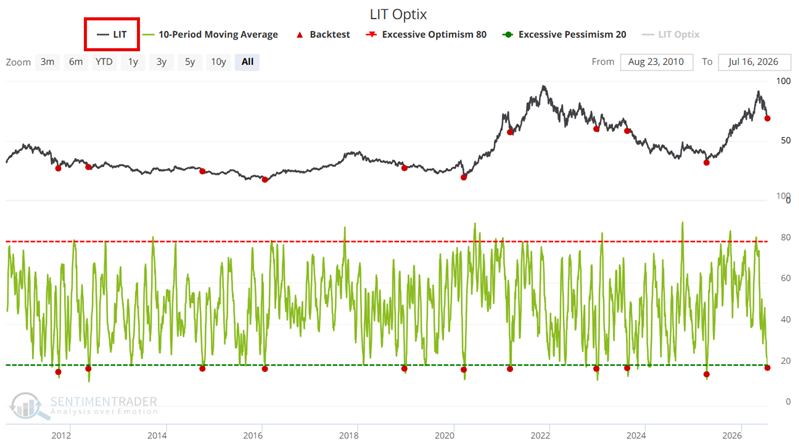

Some market relationships cannot be explained - and are therefore understandably dismissed by many individuals. But under the category of "opportunity is where you find it," consider the curious - and heretofore highly useful - relationship between trader sentiment on Lithium (Yes, Lithium) and gold and stocks, and decide for yourself.