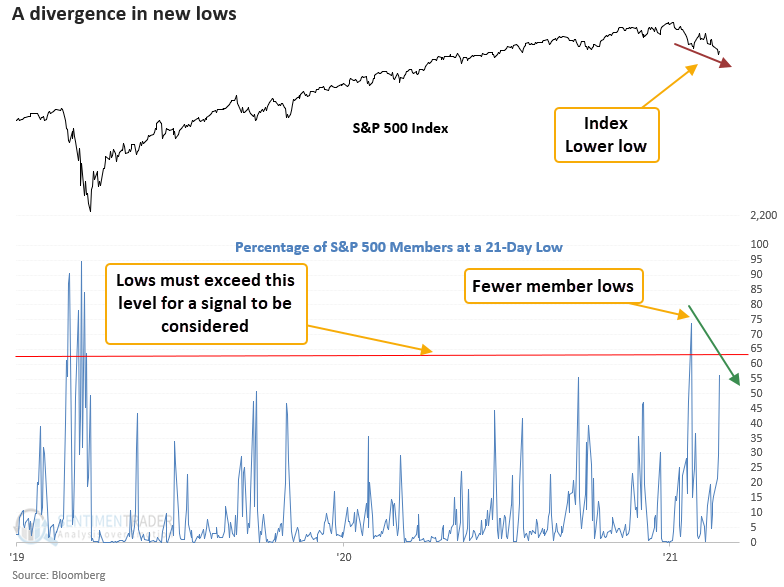

A divergence in new lows suggests the market can bounce

Key points:

- On 1/24/22, 21-day lows for S&P 500 members surged to 73%

- This week, 21-day lows for S&P 500 members reached 56% as the index registered a lower low

- Similar divergences in breadth preceded positive returns in the near term

News lows are one of the better market breadth indicators for identifying a low

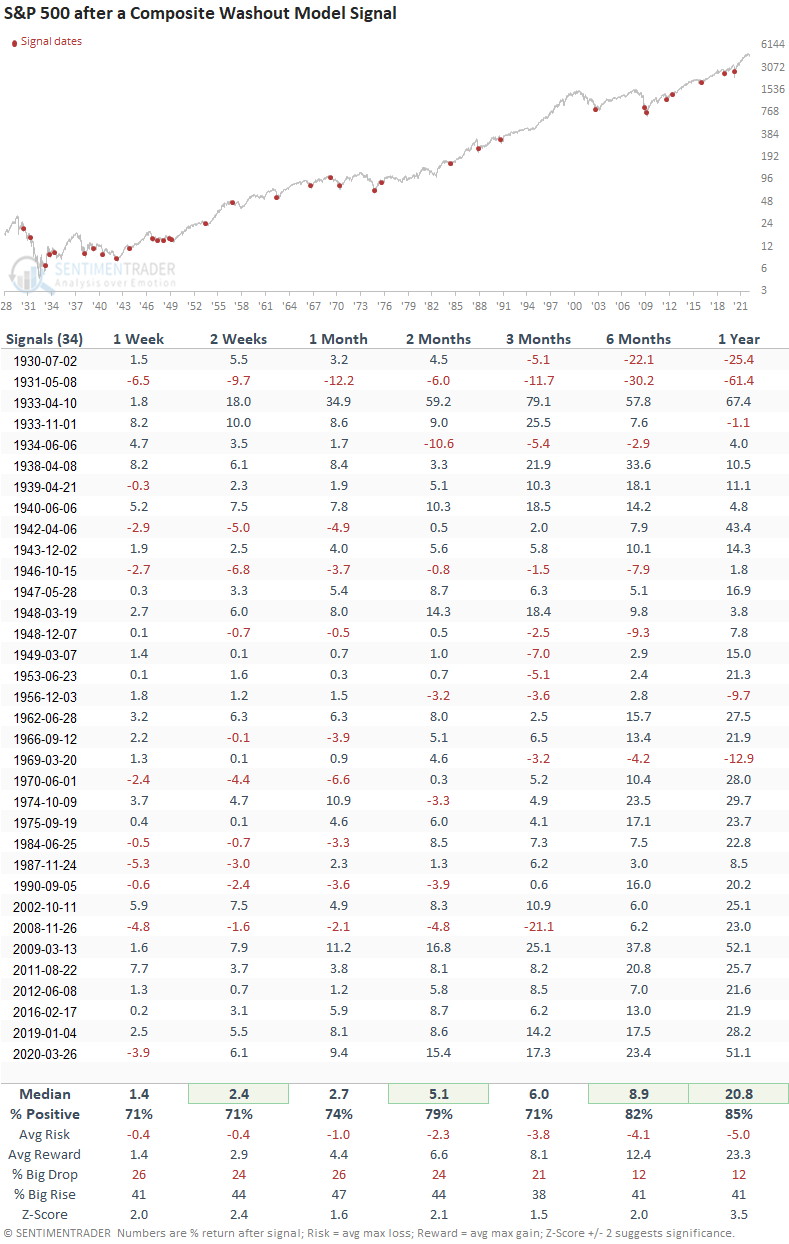

A new signal from a voting member in the composite washout model triggered an alert on Wednesday. The component is called the percentage of members at a 21-day low divergence model.

The new low divergence signal identifies when the percentage of S&P 500 members registering a new 21-day low contract as the index records a lower low. The lower low must also be a 100-day low for the index. Finally, new lows must exceed 62% before an alert can trigger. The threshold levels are high because I wanted to identify significant correction or bear market signals.

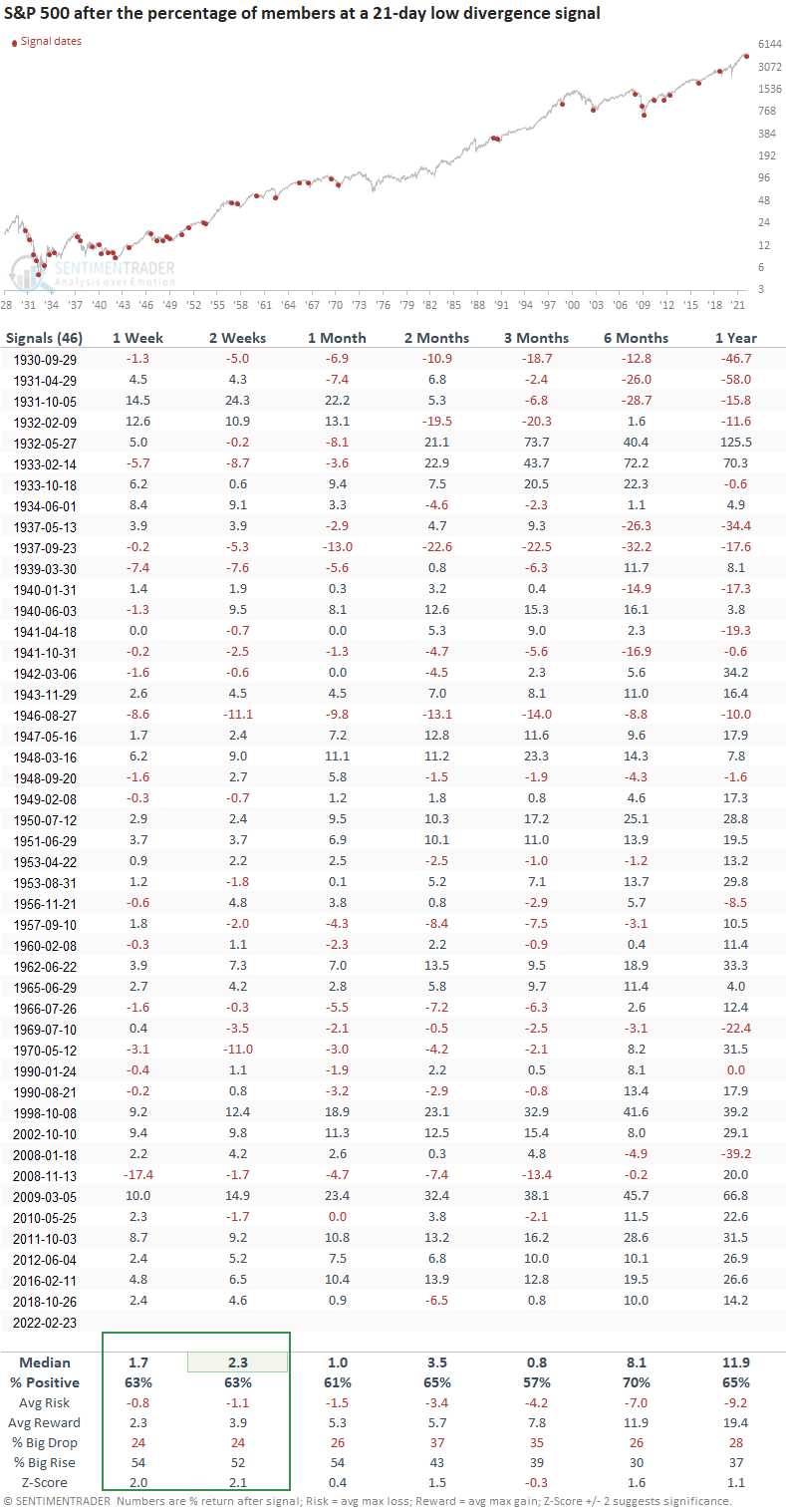

Similar signals preceded positive gains in the near term

This signal has triggered 46 other times over the past 92 years. After the others, S&P 500 future returns and win rates were favorable in the short term, with the best risk/reward profile in the 2-week window. Besides the 3-month window, the medium and long-term results and win rates look slightly better than historical averages. The challenging 1929-49 period shows an abundance of unfavorable signals.

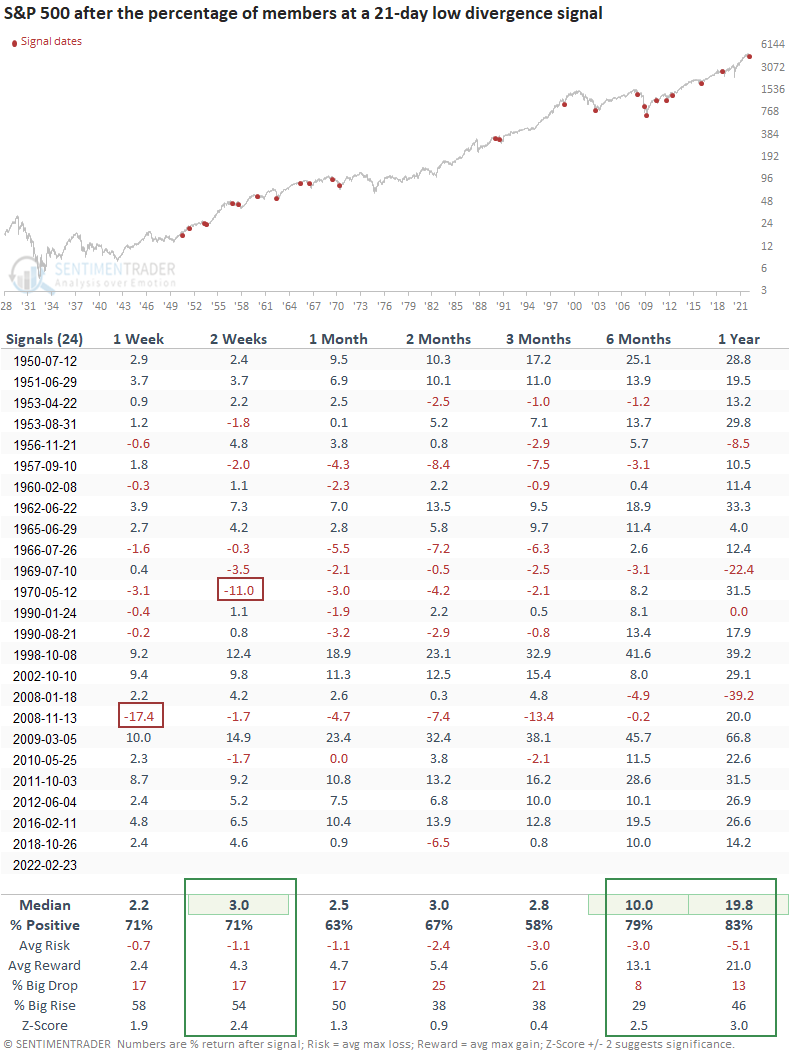

Signals since 1950 show a more favorable outlook

If we review the post-1950 period, the outlook table shows better results, win rates, and risk/reward profiles, especially the 6 and 12 months time frames. Except for the 1970 and 2008 signals, the 1 & 2-week windows show minimal drawdowns.

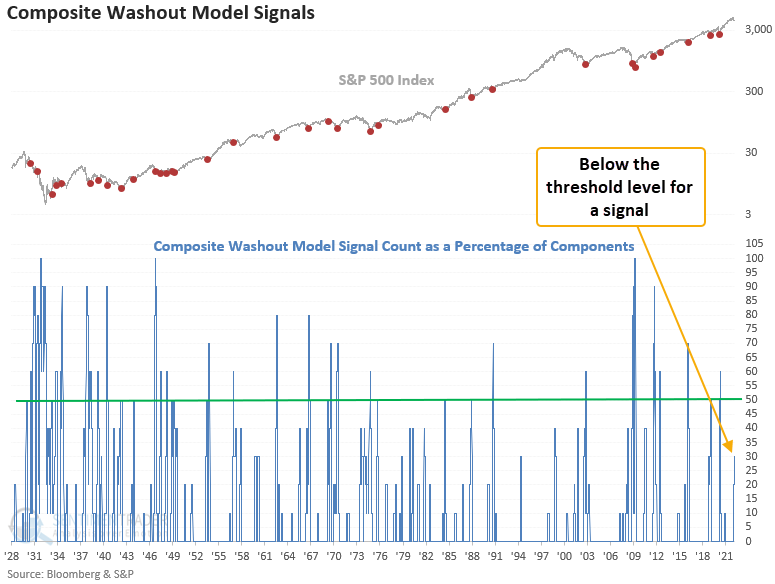

Where does the composite washout model count stand

The TCTM CWM signal count as a percentage of components now stands at 30% after the new low divergence alert. A washout signal occurs when the count reaches 50% or more, and the 10-day rate of change for the S&P 500 turns positive within 15 days of the cross above the signal threshold. i.e., index momentum is positive. I never want to catch a falling knife.

The CWM utilizes the same concept for 63 and 252-day lows. Historically, significant market lows occur after at least 2 out of 3 duration lengths trigger a signal. If you were wondering, the 63 and 252-day components have not reached the initial threshold level that creates the divergence signal. They need to surpass 48% and 32%, respectively.

Composite washout model signal performance

The composite washout model signal performance shows why I prefer a weight-of-the-evidence approach versus relying on a single indicator.

What the research tells us...

A market divergence signal occurs when S&P 500 new lows contract as the index falls to a lower low. Typically, this internal healing process is found near significant market lows, leading to higher stock prices. Similar setups to what we're seeing now have preceded rising stock prices, especially in the 2-week window. A review of post-1950 signals suggests a brighter outlook across all time frames. However, the composite washout model signal count remains below the alert threshold. CWM signals provide better returns with less risk.