Bond sentiment has bottomed after a bout of panic

Key points:

- Sentiment on bonds reached a pessimistic extreme in November and has potentially troughed

- Other indicators show extreme skepticism that bond prices can rise substantially

- These signs have a decent record of delivering positive returns for Treasury bond prices

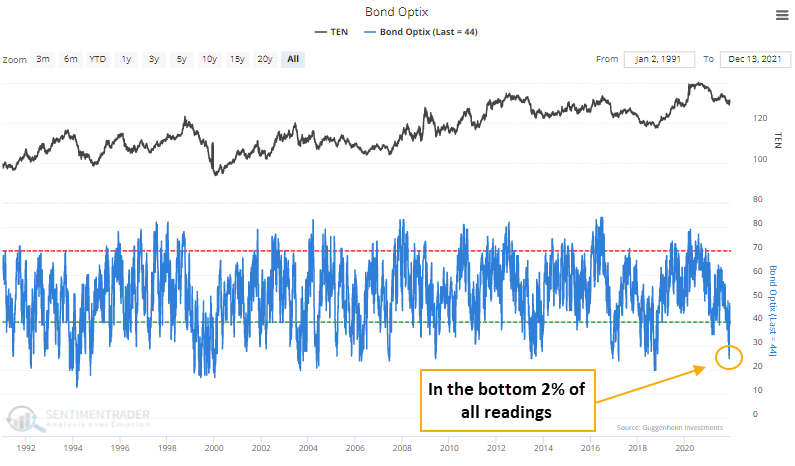

Recent optimism was in the bottom 2% of days

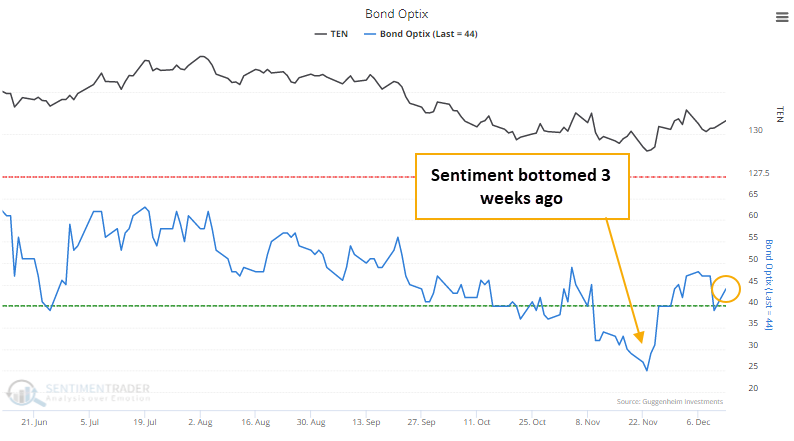

Investors ditched bonds a few weeks ago, and now they're gingerly coming back.

The Optimism Index (Optix) for bonds plunged to 25% in late November. Since then, it has rebounded and not set another low, raising the possibility that sentiment has troughed.

That heavy pessimism from before Thanksgiving was in the bottom 2% of all days in the past 30 years.

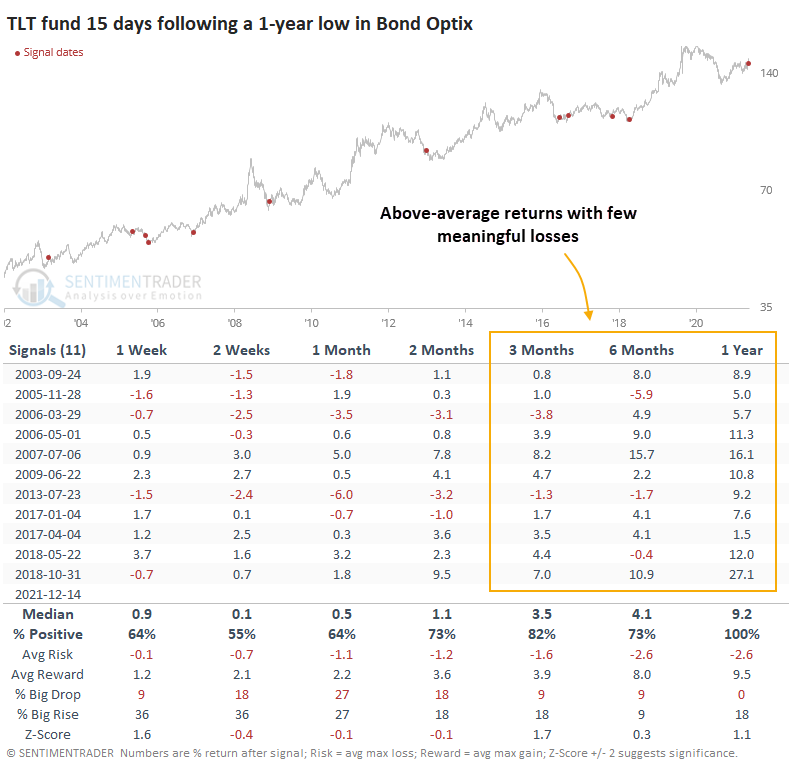

Let's make the assumption that not setting a lower low in sentiment for 15 consecutive days, after recording a reading below 30%, suggests that investors have finished panicking. Then we can see if that improved forward returns. For 10-year Treasury futures, it did, but only modestly.

The problem was multiple false positives during a couple of big drops in bonds in the mid-and late-1990s. When we switch to the TLT fund, returns were excellent in large part because it avoided those ugly episodes.

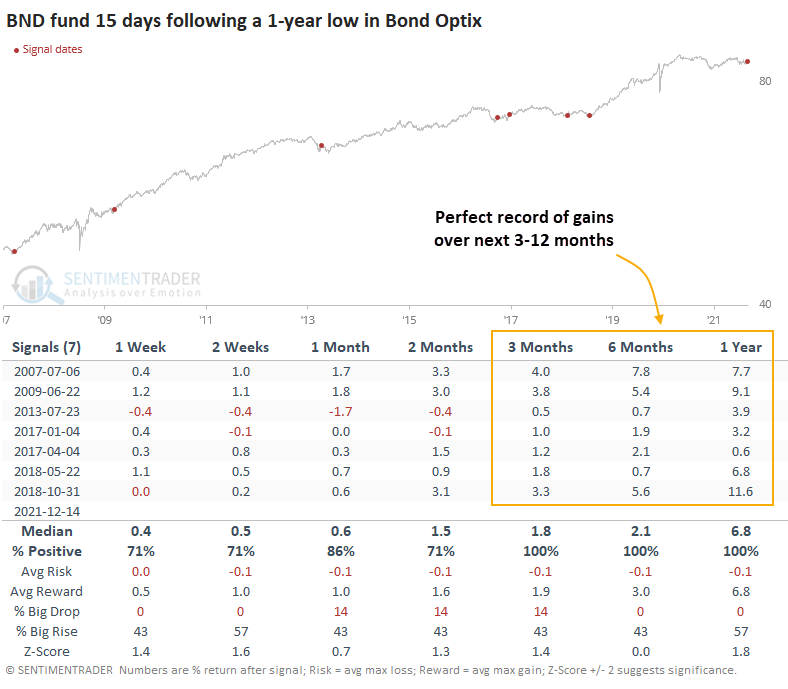

The BND fund has even less history but is a broader fund though still heavily influenced by the action in Treasuries.

Other measures show skepticism

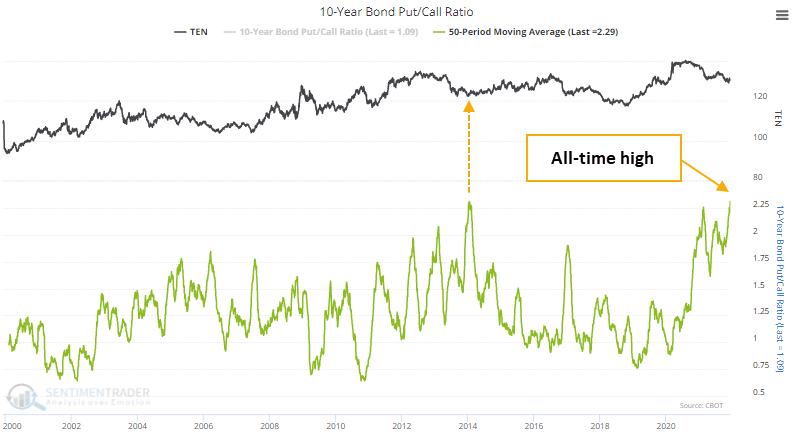

Looking at some other measures of sentiment toward bonds, a 50-day average of the put/call ratio on 10-year Treasury futures just ticked up to an all-time high. That exceeds the prior record from January 2014, which preceded a 2.5-year run in Treasuries.

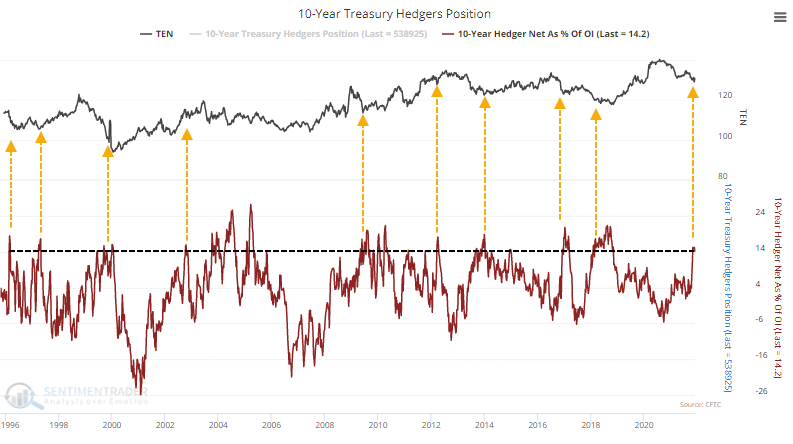

At the same time, "smart money" commercial hedgers are holding more than 14% of open interest in 10-year Treasury futures net long, among their most significant exposures ever.

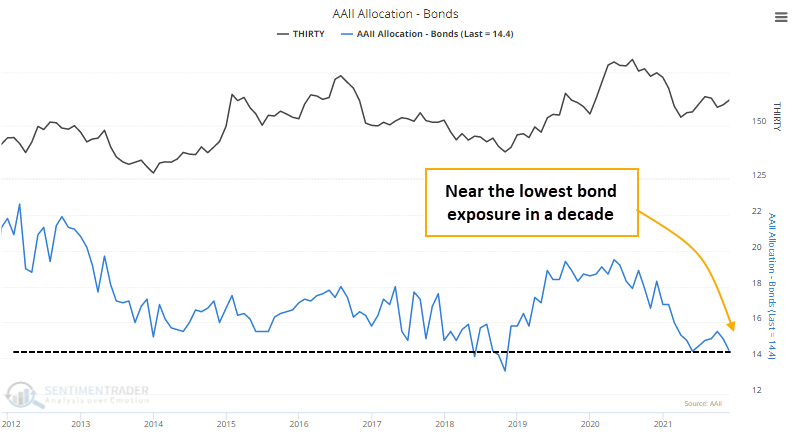

Surveys show little appetite for bonds, as investors are bombarded with the narrative about the dangers of holding fixed income securities during a period of high inflation. Individual investors are holding nearly a decade-low exposure to bonds at 14.4% of their portfolios. Before the last decade, they sometimes held less than 10% of their portfolios in bonds, so it can get quite a bit lower.

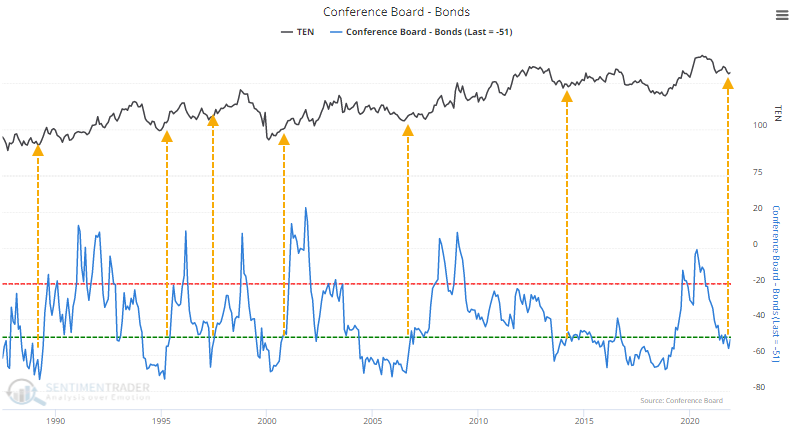

Similarly, U.S. consumers are pessimistic on bonds. More than 62% of consumers expect interest rates to rise (bond prices fall), while only 11% expect rates to drop (bond prices rise). Recent readings have been in the bottom 25% of all months since 1988.

None of these are perfect but generally precede rising bond prices after similar readings. The biggest challenge, as usual, is whether the environment we face now is anything like any other period in history, much less just the past 30 years.

What the research tells us...

We don't try to guess future macroeconomic conditions or their likely impact on markets. Instead, we focus on what's happening right now and how investors react to it. And those indications are that investors are anxious about the potential for rising rates, as they hold few bonds relative to other assets and are hedging against further declines in bond prices. Sentiment has recovered from the extreme pessimism of a few weeks ago, suggesting the latest mini-panic has subsided. While fundamental forces can always overwhelm any technical extremes, the past 20 years of similar behavior preceded medium-term gains for broad bond funds.