Commodity Bulls Hope for a 1973 Repeat

On Tuesday, we saw that the 4-month start to stocks this year has had some impressive precedents. While most of the similar years witnessed some consolidation during the summer months, the long-term implications were positive.

Commodities have arguably had an even more impressive start. The long-term trend in stocks is well-documented to be higher as companies innovate and produce profits, but commodities are much more cyclical. As prices rise, farmers plant more crops, or miners dig more stuff out of the ground, and prices go down. It's hard to sustain uptrends except when there is a massive supply/demand imbalance.

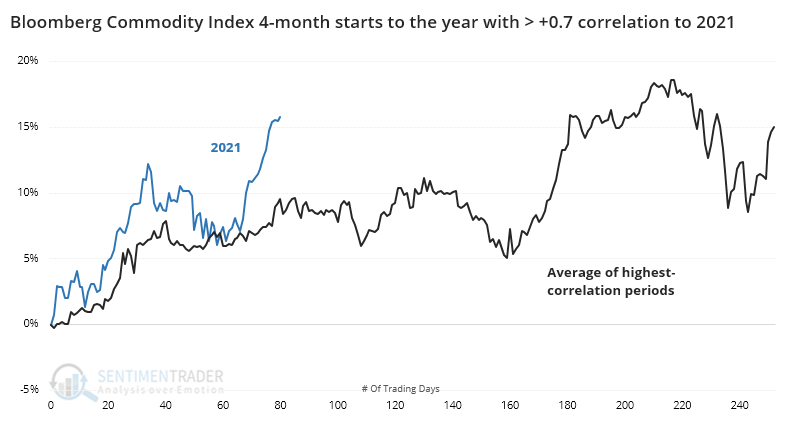

MOST SIMILAR 4-MONTH STARTS FOR COMMODITIES

Through late April, the Bloomberg Commodity Index showed a gain well into the double-digits, and it has only added to them since then. Using the same methodology we used for stocks, we see that 9 other years had a correlation greater than +0.7 (on a scale of -1.0 to +1.0) through the first 4 months of the year.

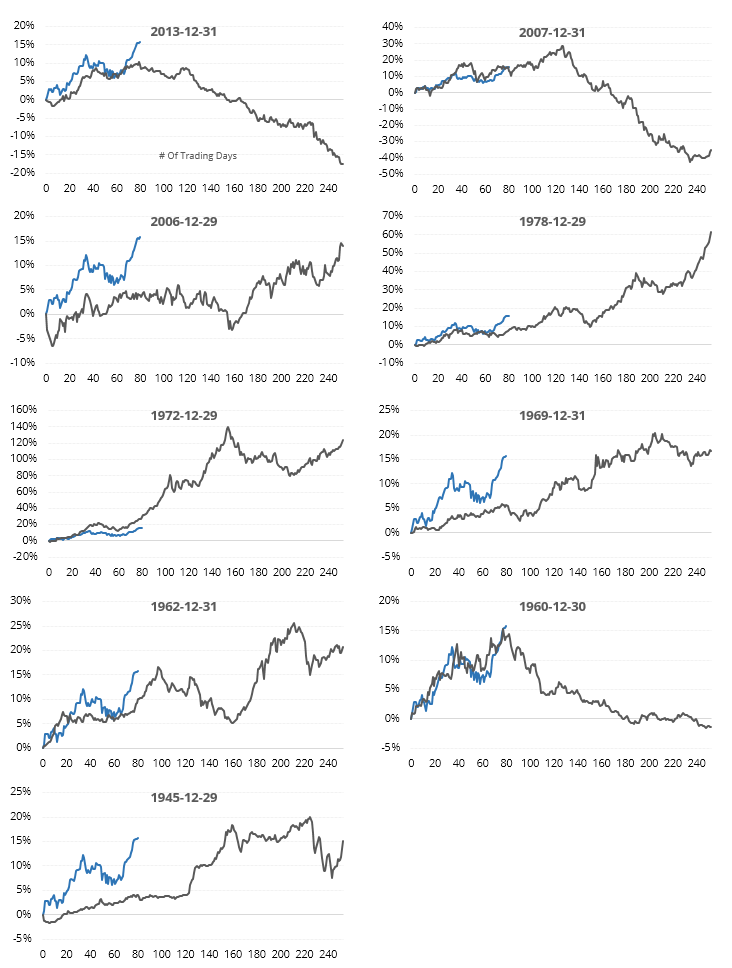

The years all showed gains through April and enjoyed a roughly similar path to get there, but the only year with a better 4-month beginning was 1973. Commodity bulls would love to see a repeat, as it preceded massive additional gains.

Even though their correlations to 2021 were all highly positive, there was still quite a bit of variability among the samples, especially in terms of magnitude. There was a general tendency to see commodities peak at about this point in the year, though.

WHAT GOOD STARTS MEAN FOR THE REST OF THE YEAR

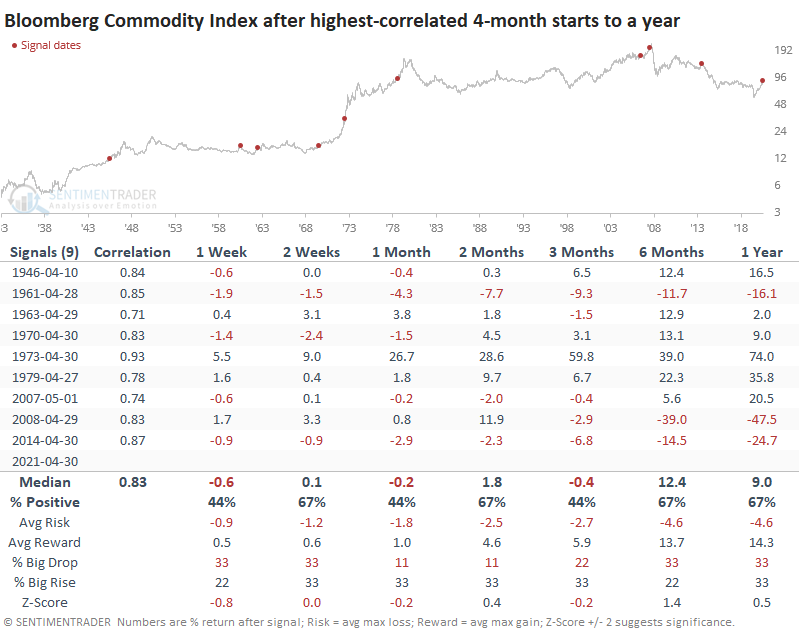

The table below shows future returns in the index from the end of April for those years with the highest correlation to 2021.

The year with the highest correlation was 1973, and there was virtually no letup as it preceded massive and sustained gains in the index. Among the others, only 1979 saw no negative returns across all time frames.

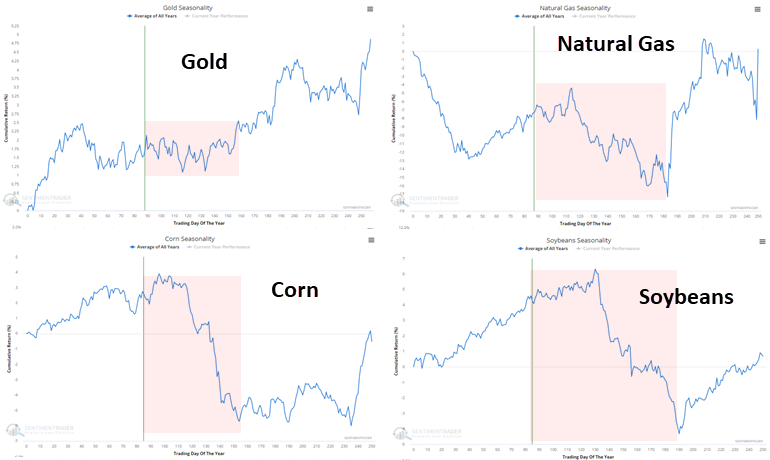

There are some shorter-term challenges to those precedents. The chart above clearly shows that the summer months preceded some choppy trading for commodities. Among some of the largest influences on the Bloomberg Commodity Index, the seasonal windows for gold, natural gas, corn, and soybeans are questionable.

Likewise, when we looked at the rates of change in commodities in March and April, we saw just how tough it has been for this market to sustain massive gains over the medium-term.

So, commodities should pause over the next few months and digest their recent gains. As always, a market that doesn't do what it should gives us a strong hint that something structural has changed, and this market has already done that to some degree. If commodities follow the 1973 playbook, then we won't see much, if any, weakness in the weeks and months to come. But it will have to fight historical analogs, seasonality, momentum, and sentiment, all pointing to a pause.