Credit investors are getting a bit nervous

Much of the rally in assets over the past few months seems to have been driven by ever-easier financial conditions.

Granted, that is a bit tautological, since rising asset prices help drive financial conditions but the performance of the S&P 500 is only 1 of 9 inputs to the Bloomberg U.S. Financial Conditions Index, for example.

After the spike a year ago, financial conditions have steadily eased. Only lately have they plateaued (or troughed, depending on which index you're looking at).

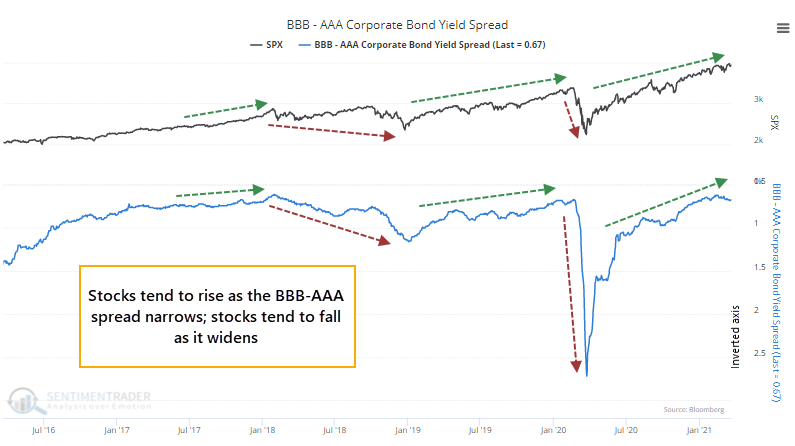

Part of this is due to changes within the bond market. It's no secret that bonds have gotten shellacked, even corporate bonds. And within that universe, we're just now seeing the spread between the lowest-rated investment-grade corporate bonds rising faster than that of the highest-rated bonds. This suggests that credit investors are starting to get just a bit nervous.

There could be other reasons, like outlooks for taxes rates, liquidity, sales geography, etc., that are influencing this, but generally, we can assume that when the spread between lower-quality and high-quality bonds is rising, it's during times of rising anxiety. The chart below shows this clearly (note that the scale on the spread is inverted).

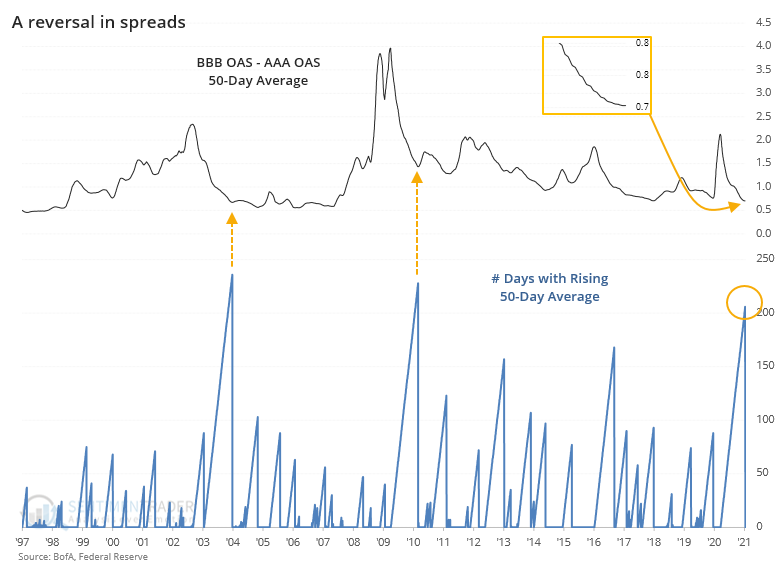

For the first time in almost a year, spreads on riskier bonds are starting to rise compared to spreads on the safest ones. It had been more than 200 days since the 50-day average of the spread was rising, ending the 3rd-longest streak in 25 years.

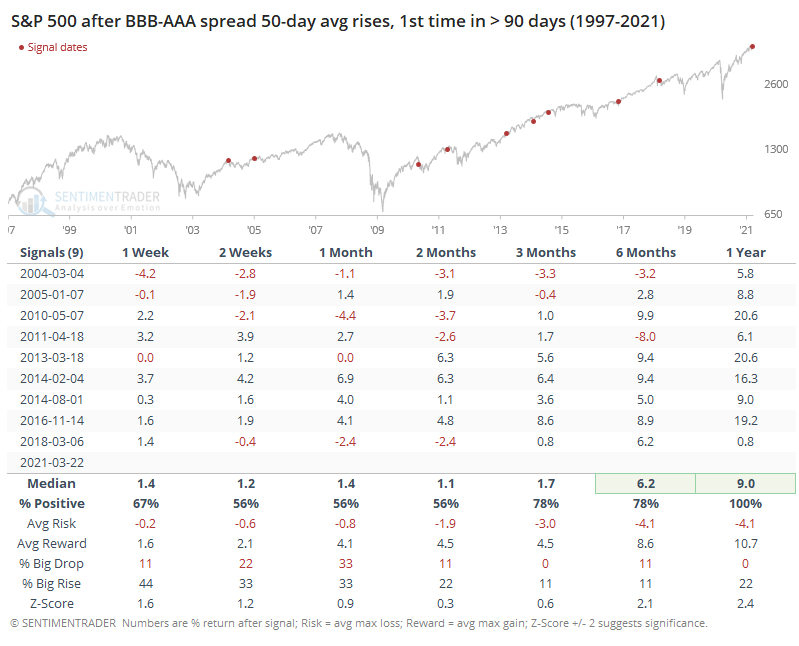

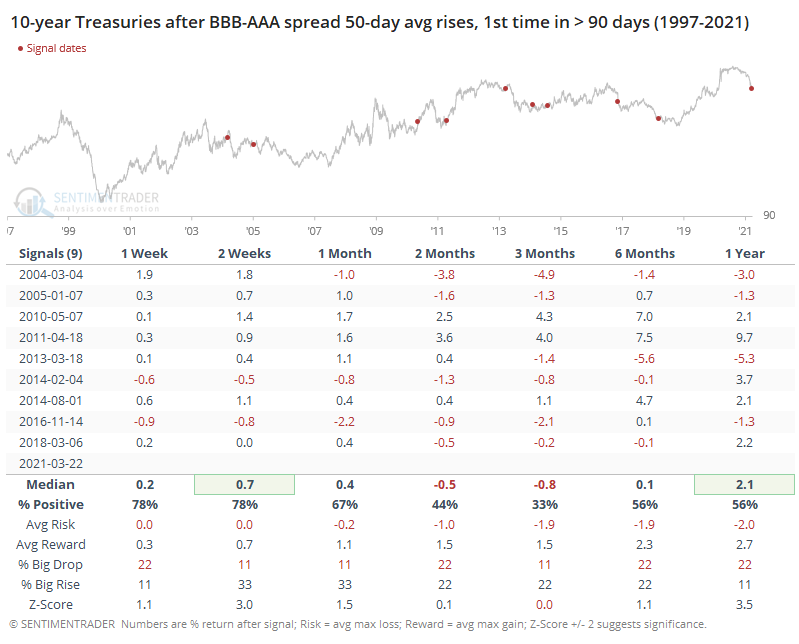

When the 50-day average of this difference in spreads first started to rise after more than 90 days of declining, it wasn't necessarily a sell signal for stocks. Returns over the medium-term were mediocre, about in line with random. Thanks to the overall rising trend over the study period, longer-term returns were good.

After the ends of the two other 200+ day streaks, in March 2004 and May 2010, the S&P did struggle more over the ensuing weeks and months. Those time frames also lined up with what had been protracted extremes in optimistic sentiment like we're seeing now.

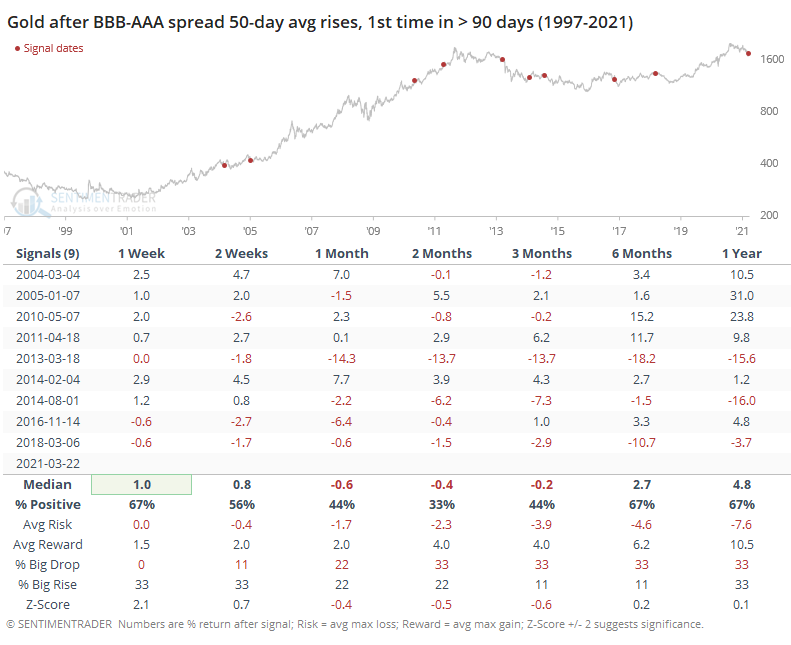

It might be assumed that if credit investors were becoming more nervous, then they might bid up some safe-haven assets. Gold, however, did not react well.

There also wasn't much of a flight-to-safety response in Treasuries.

The idea that credit investors seem to be getting a tad more nervous, as we're in the midst of one of the most protracted bouts of extremely optimistic sentiment in over 20 years, is a modest worry. It's not like spreads are blowing out, and the other two times we saw a similar situation, stocks only declined modestly. It's just another indication that the risk/reward for riskier assets isn't all that great right now.