Headlines

|

|

Buying the Dips in SPY doesn't have to be rocket science:

Investors often hear of traders "buying the dips," i.e., putting money into the market when it pulls back in price. Can this approach to trading work? And can it be done without applying complex algorithms? This piece argues that the answers are "Yes" and "Yes."

Bottom Line:

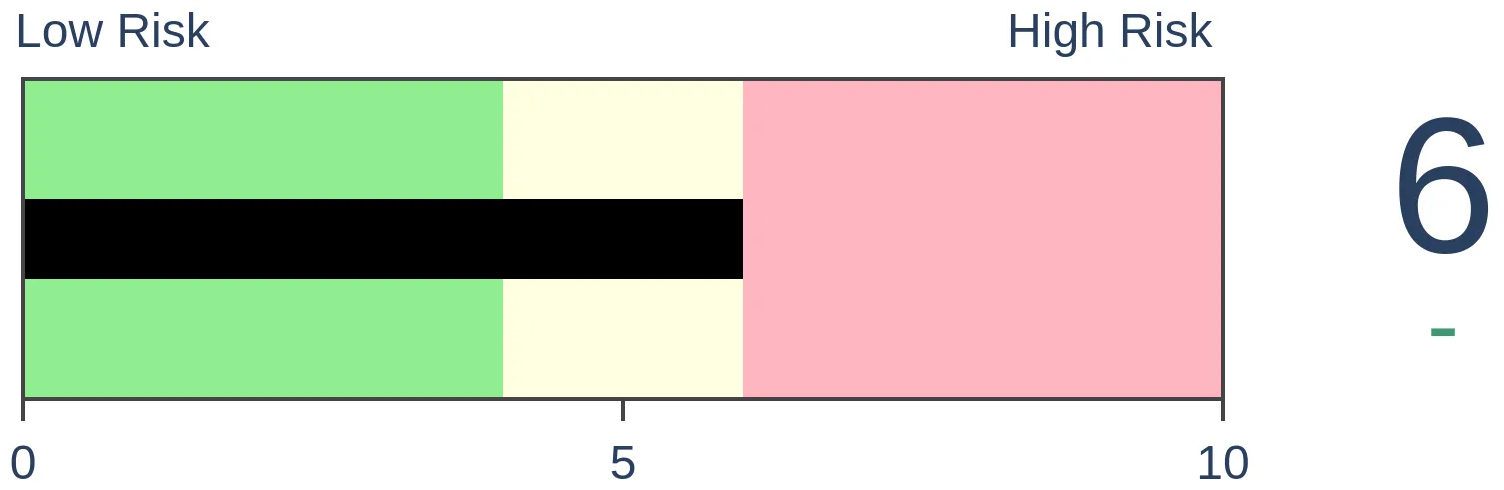

STOCKS: Hold By early October, sentiment had reset. Several important momentum streaks ended, which has brought in buyers in the past, and seasonality turned positive. We're now seeing signs that sentiment has quickly shifted, especially among options traders. It's gotten to an extreme that has preceded weaker-than-average returns.

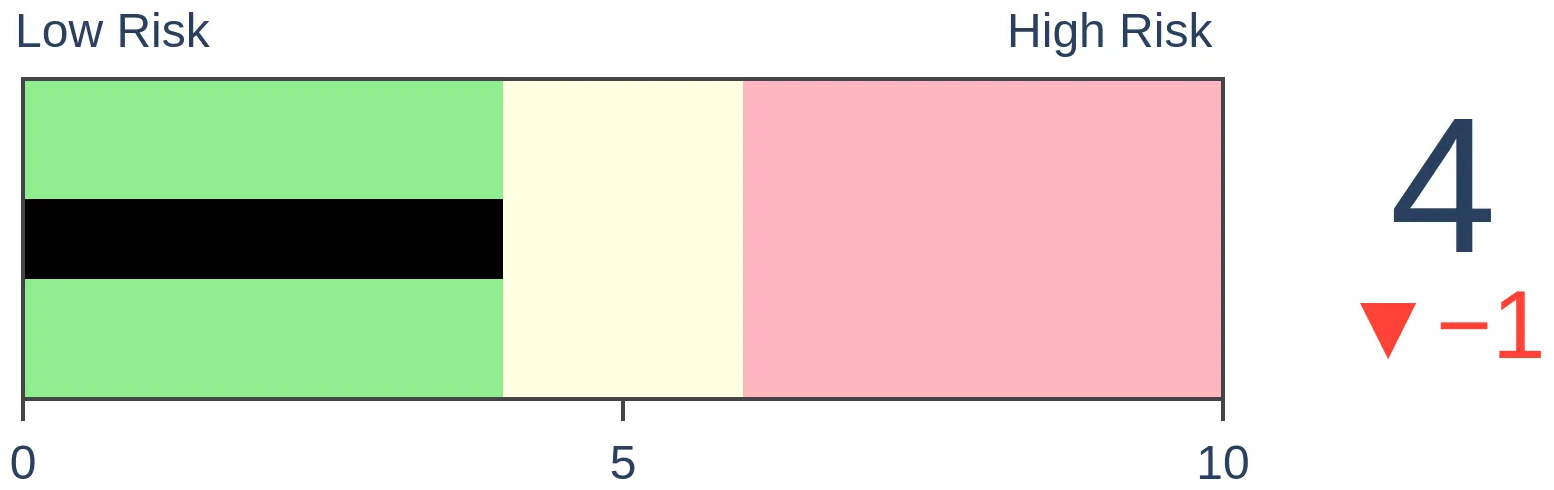

BONDS: Hold In late October, sentiment on bonds - from Treasuries to corporates - entered pessimistic territory. It's now starting to recover, with some quick moves in corporate bonds. We'll see if those bonds, in particular, can hold recent gains.

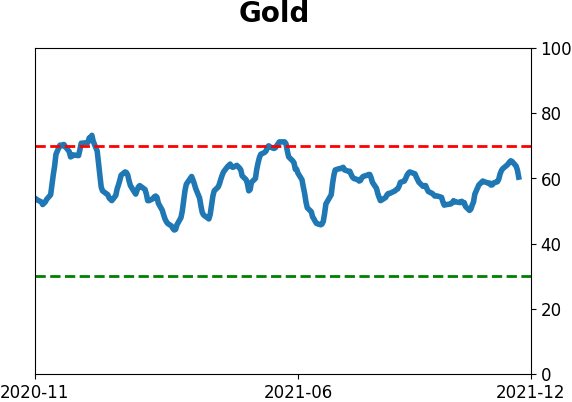

GOLD: Hold

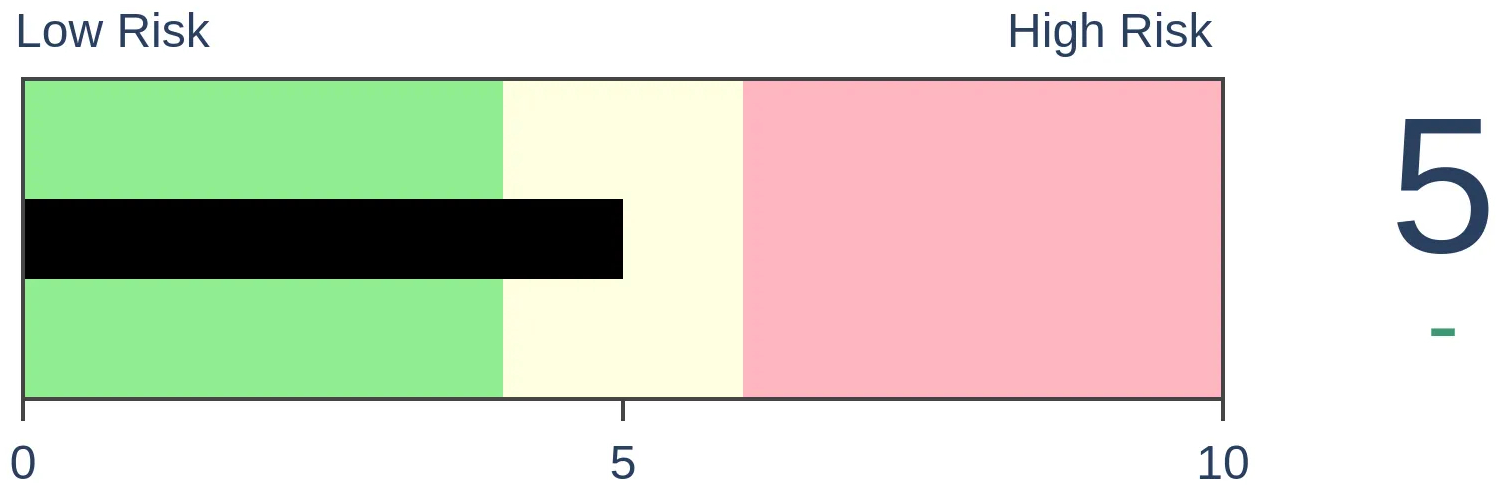

Gold and miners were rejected after trying to recover above their 200-day averages in May. Some oversold extremes in breadth measures among miners triggered in late September, and they've recovered a bit since then. The group still has some proving to do.

|

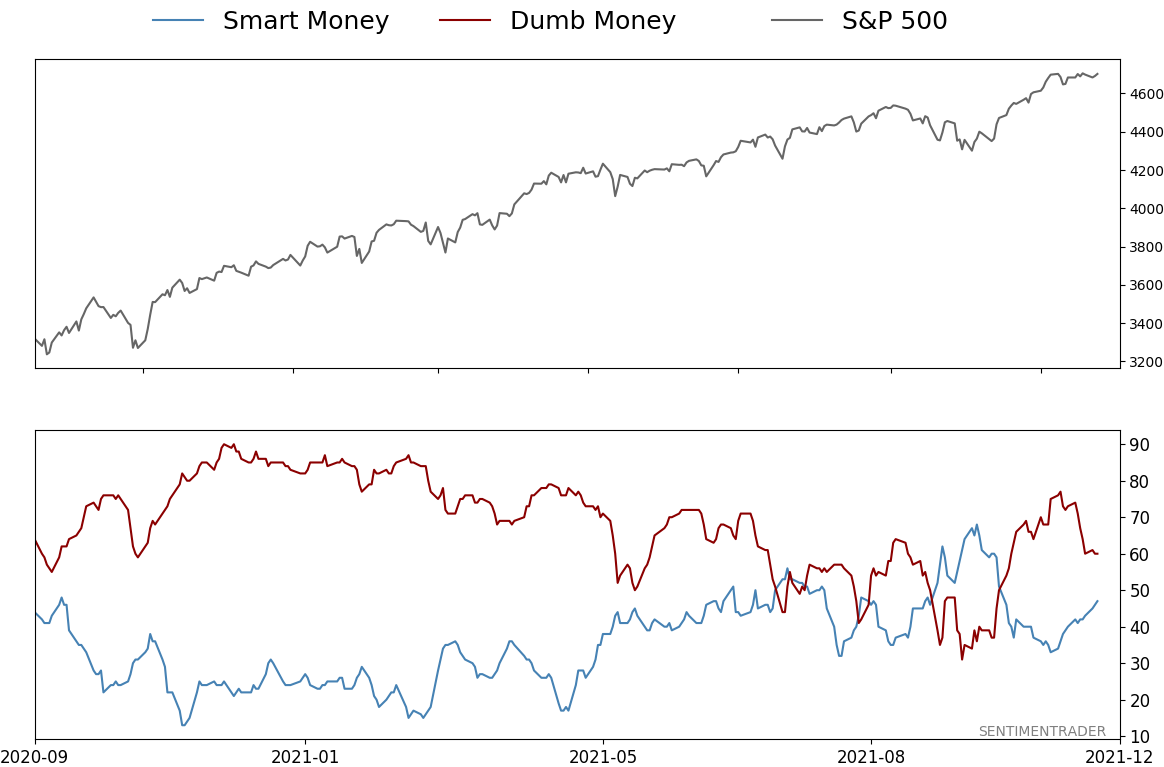

Smart / Dumb Money Confidence

|

Smart Money Confidence: 47%

Dumb Money Confidence: 60%

|

|

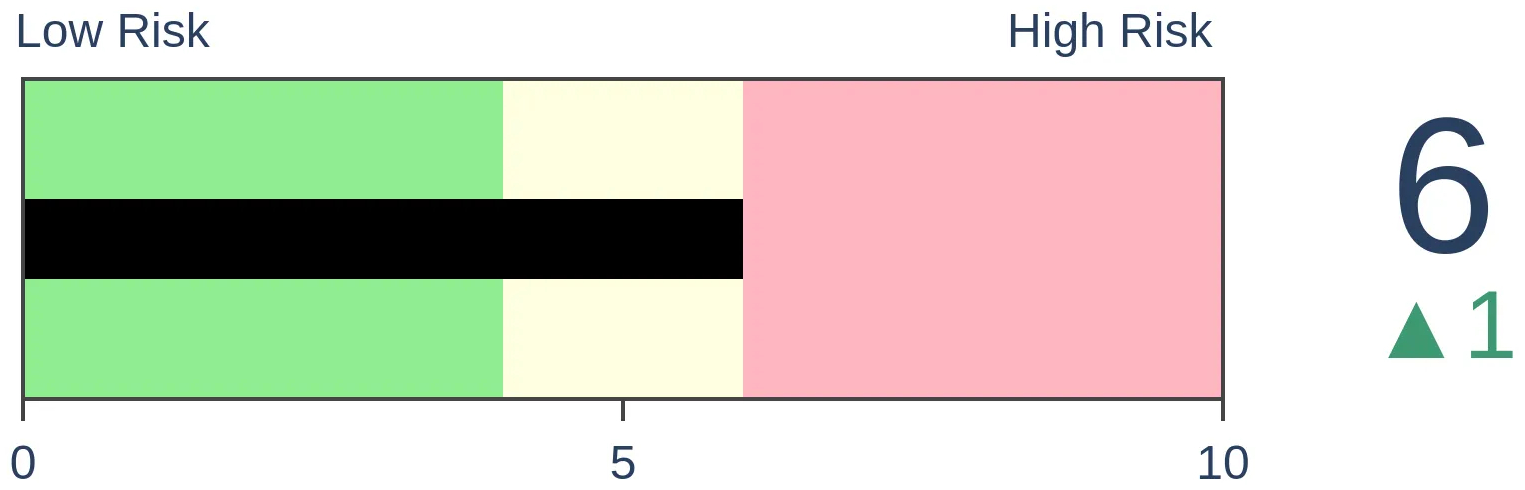

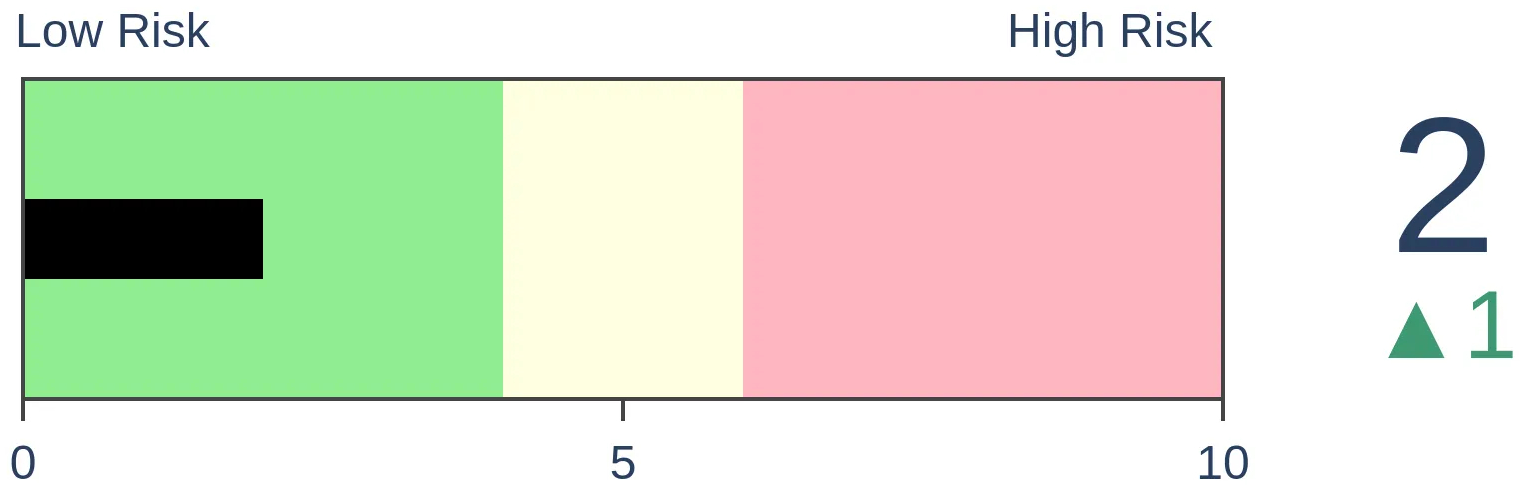

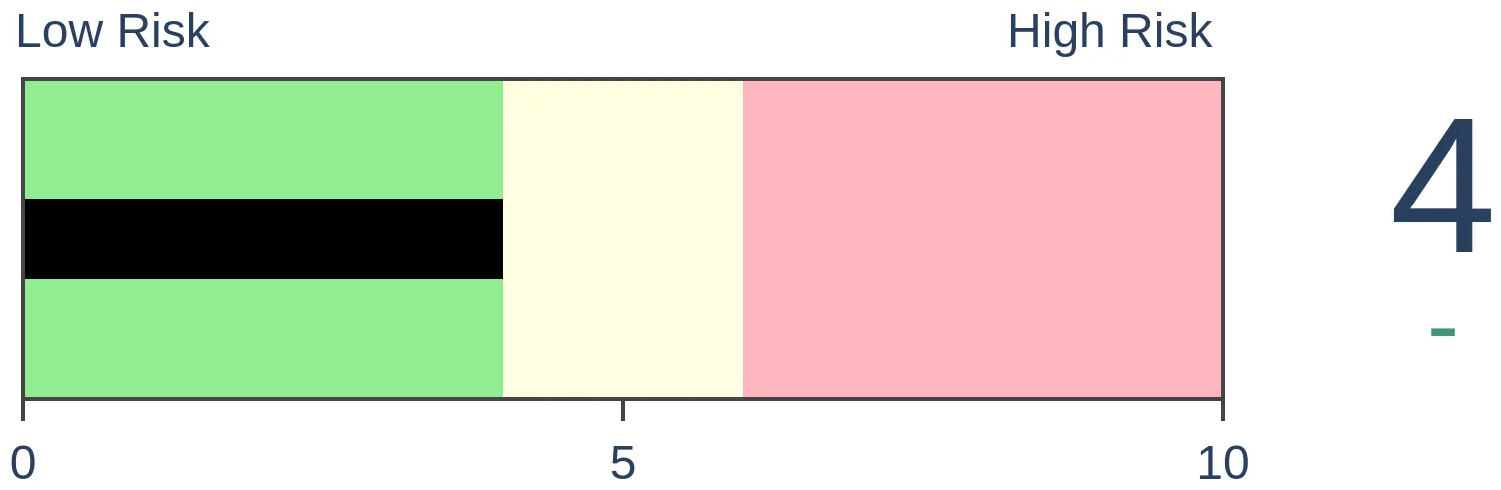

Risk Levels

Stocks Short-Term

|

Stocks Medium-Term

|

|

Bonds

|

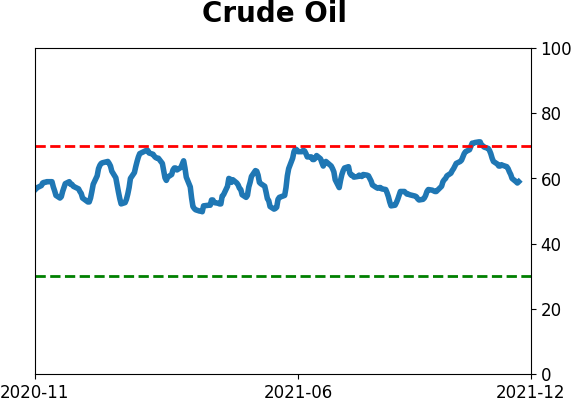

Crude Oil

|

|

Gold

|

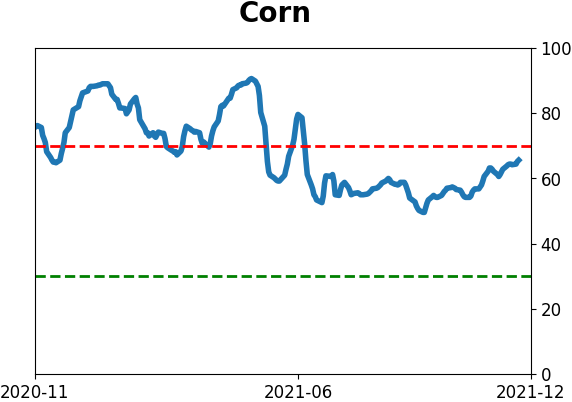

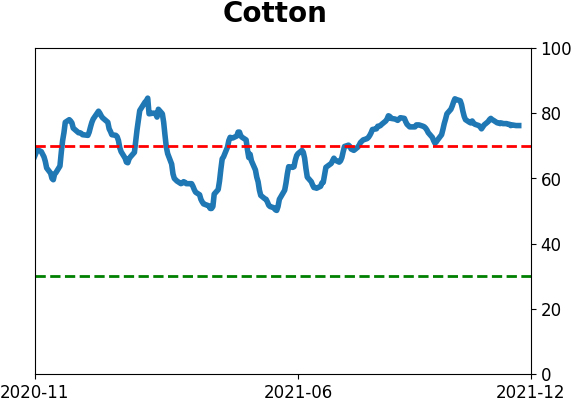

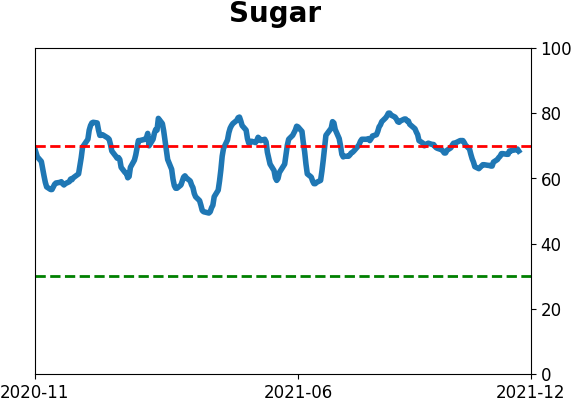

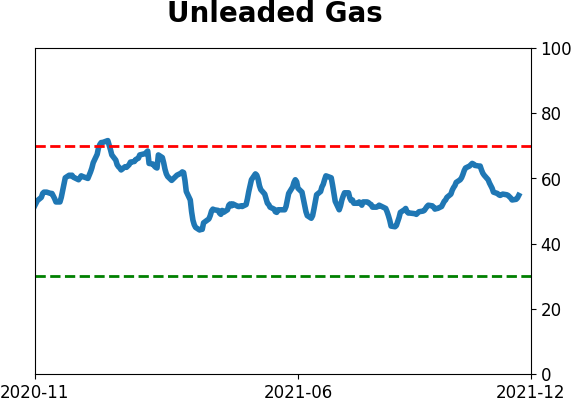

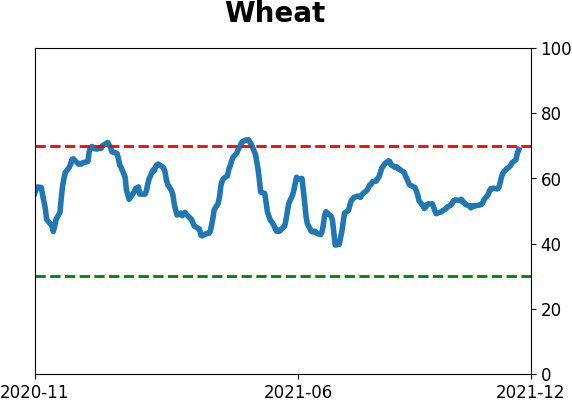

Agriculture

|

|

Research

By Jay Kaeppel

BOTTOM LINE

Investors often hear of traders "buying the dips," i.e., putting money into the market when it pulls back in price. Can this approach to trading work? And can it be done without applying complex algorithms? This piece argues that the answers are "Yes" and "Yes."

FORECAST / TIMEFRAME

None

|

Key Points

- In a perfect world, buying dips in an ongoing uptrend should be a winning strategy

- Finding the "exactly right" moment to buy is an admirable goal, but real-world trading tends to be a lot messier than most of us would hope

- Ultimately, position sizing and risk management are just as (maybe more?) important than market timing

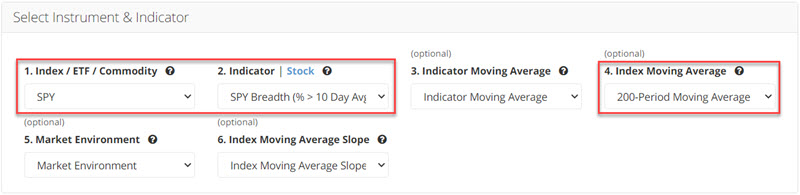

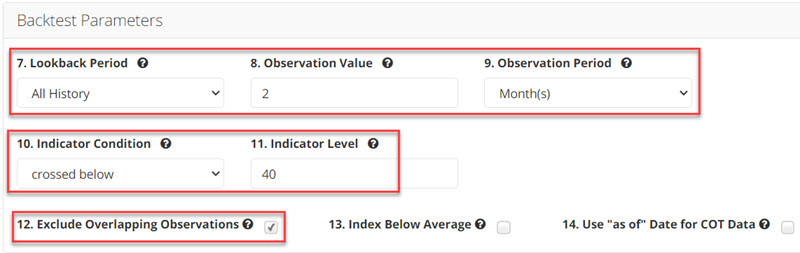

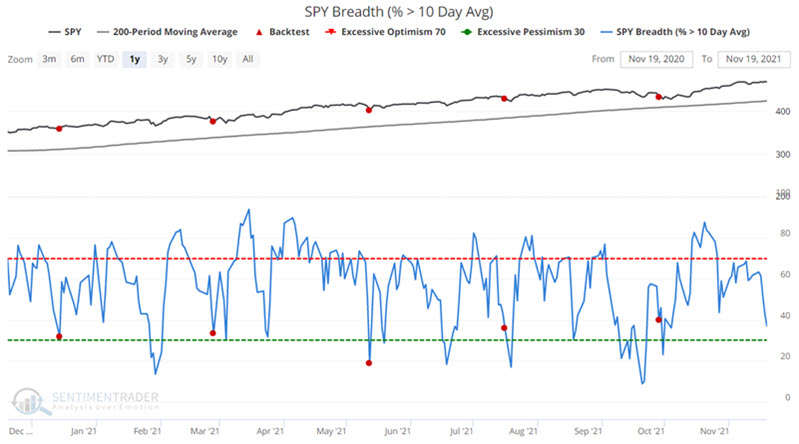

SPY Breadth Signal

Let's consider the potential for using a simple breadth-based indicator to play the long side using shares of ETF ticker SPY (SPDR S&P 500 ETF Trust ). The rules we will use are:

- SPY > 200-day moving average

- SPY Breadth (% > 10 Day Avg) crosses below 40%

- For the first time in 2 months

The first condition filters for an objective "uptrend." The second condition objectively identifies a pullback in the overall index. The input screens appear below. You can run this test by clicking here.

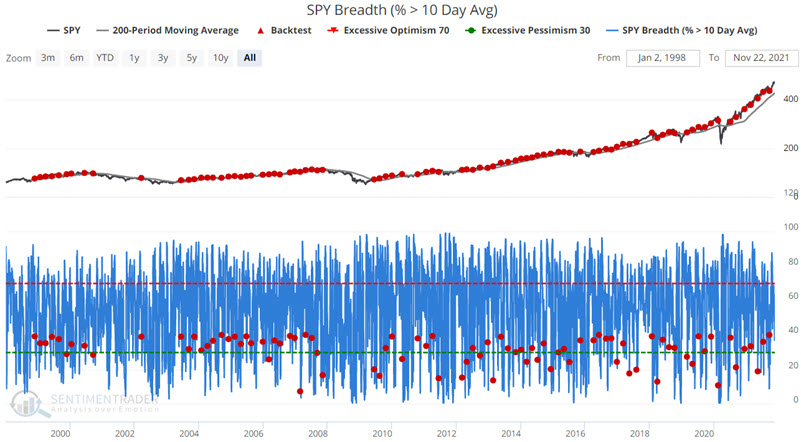

The Signals

The signals generated by the rules above appear in the chart below.

There is no shortage of trading signals. The summary of results appears below. For our purpose, we will focus on the 2-month time frame.

The chart zooms in on the chart above and below displays the signals generated in the past year.

Applying to Real-World Trading

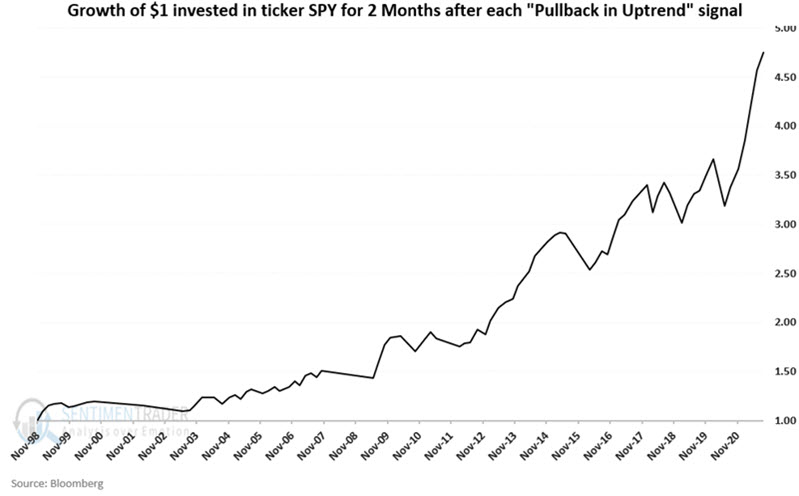

Since 11/30/1998, there have been 87 signals, including the most recent open signal triggered on 9/28/2021. No new signal can be generated before 11/28/2021.

Let's run the following hypothetical test:

- Allocate a specific starting amount to this strategy

- Invest all capital allocated in SPY shares on the closing date of each new signal

- Sell SPY shares two months after the initial signal date

- Repeat the steps above - reinvesting all capital - on each new signal date

The cumulative hypothetical growth of $1 invested as detailed above since 1998 appears in the chart below.

The results displayed in the chart above are by now means a "straight-line." Still, the lower left to upper right nature of the equity curve is unmistakable.

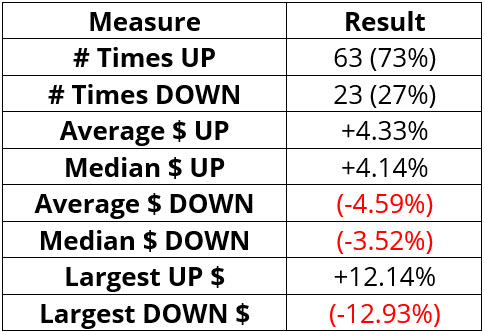

A summary of trading results appears in the table below.

The strategy detailed here is not the "be all, end all" of trading systems and can undoubtedly be improved. But note also what it does demonstrate - that a simple "buy the dips in an uptrend" approach to trading can be consistently profitable over time.

The keys to succeeding using a strategy similar to the one above are:

- Allocating only a reasonable amount of risk capital

- Having the discipline to act when each new signal occurs (i.e., filtering out all of the "noise" that can create doubt)

What the research shows…

- Trading in the direction of the primary trend is one of the easiest ways for any trader to gain an "edge" and put the odds on their side

- Buying a pullback in an ongoing uptrend is another way to increase the odds of success and improve profit potential on a trade-by-trade basis

- Allocating a reasonable percentage of one's capital - and never "betting the ranch" is the best way to ensure that you stick with a viable strategy long enough to enjoy the "edge" that the approach enjoys

Active Studies

| Time Frame | Bullish | Bearish | | Short-Term | 2 | 0 | | Medium-Term | 11 | 0 | | Long-Term | 13 | 6 |

|

Indicators at Extremes

Portfolio

| Position | Description | Weight % | Added / Reduced | Date | | Stocks | RSP | 10.7 | Added 6.4% | 2021-10-01 | | Bonds | 32.7% BND, 7.1% SCHP | 39.8 | Added 8.3% | 2021-10-26 | | Commodities | GCC | 2.4 | Reduced 2.1%

| 2020-09-04 | | Precious Metals | GDX | 4.6 | Reduced 4.2% | 2021-05-19 | | Special Situations | 9.8% KWEB, 4.7% XLE, 2.9% PSCE | 17.3 | Added 9.78% | 2021-10-01 | | Cash | | 24.1 | | |

|

Updates (Changes made today are underlined)

Much of our momentum and trend work has remained positive for several months, with some scattered exceptions. Almost all sentiment-related work has shown a poor risk/reward ratio for stocks, especially as speculation drove to record highs in exuberance in February. Much of that has worn off, and most of our models are back toward neutral levels. There isn't much to be excited about here. The same goes for bonds and even gold. Gold has been performing well lately and is back above long-term trend lines. The issue is that it has a poor record of holding onto gains when attempting a long-term trend change like this, so we'll take a wait-and-see approach. Momentum has ebbed quickly in recent weeks, and nearing oversold levels in some indicators. This can be a dangerous area, with a lot of short-term volatility, but we'd be more inclined to add medium- to long-term exposure rather than sell on much more of a decline, thanks to already rock-bottom exposure. Other areas look more attractive, including some overseas markets. RETURN YTD: 11.3% 2020: 8.1%, 2019: 12.6%, 2018: 0.6%, 2017: 3.8%, 2016: 17.1%, 2015: 9.2%, 2014: 14.5%, 2013: 2.2%, 2012: 10.8%, 2011: 16.5%, 2010: 15.3%, 2009: 23.9%, 2008: 16.2%, 2007: 7.8%

|

|

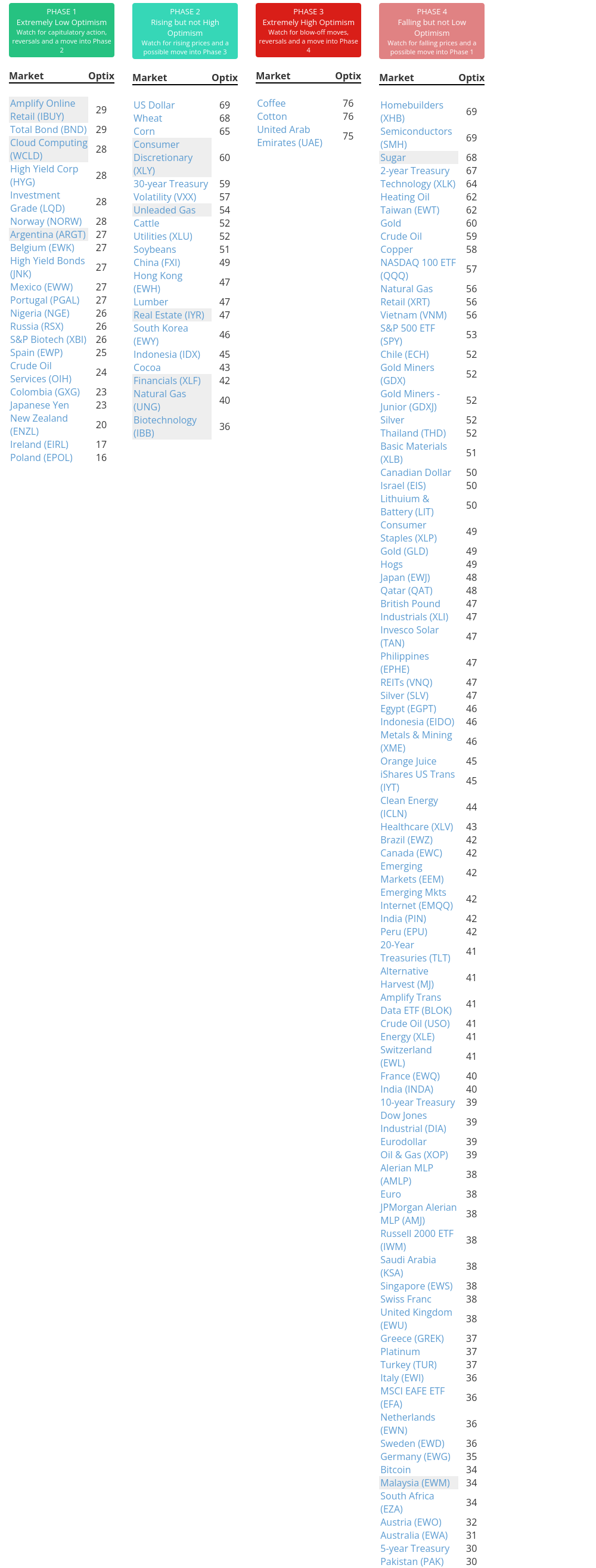

Phase Table

Ranks

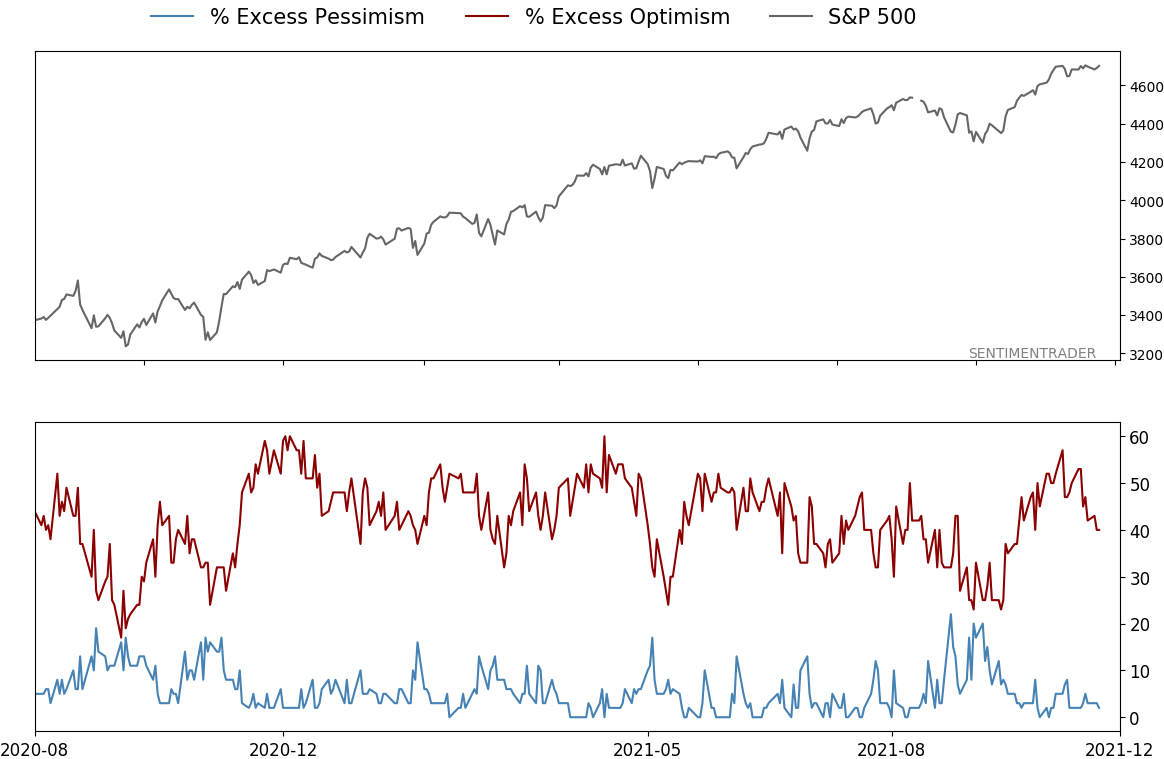

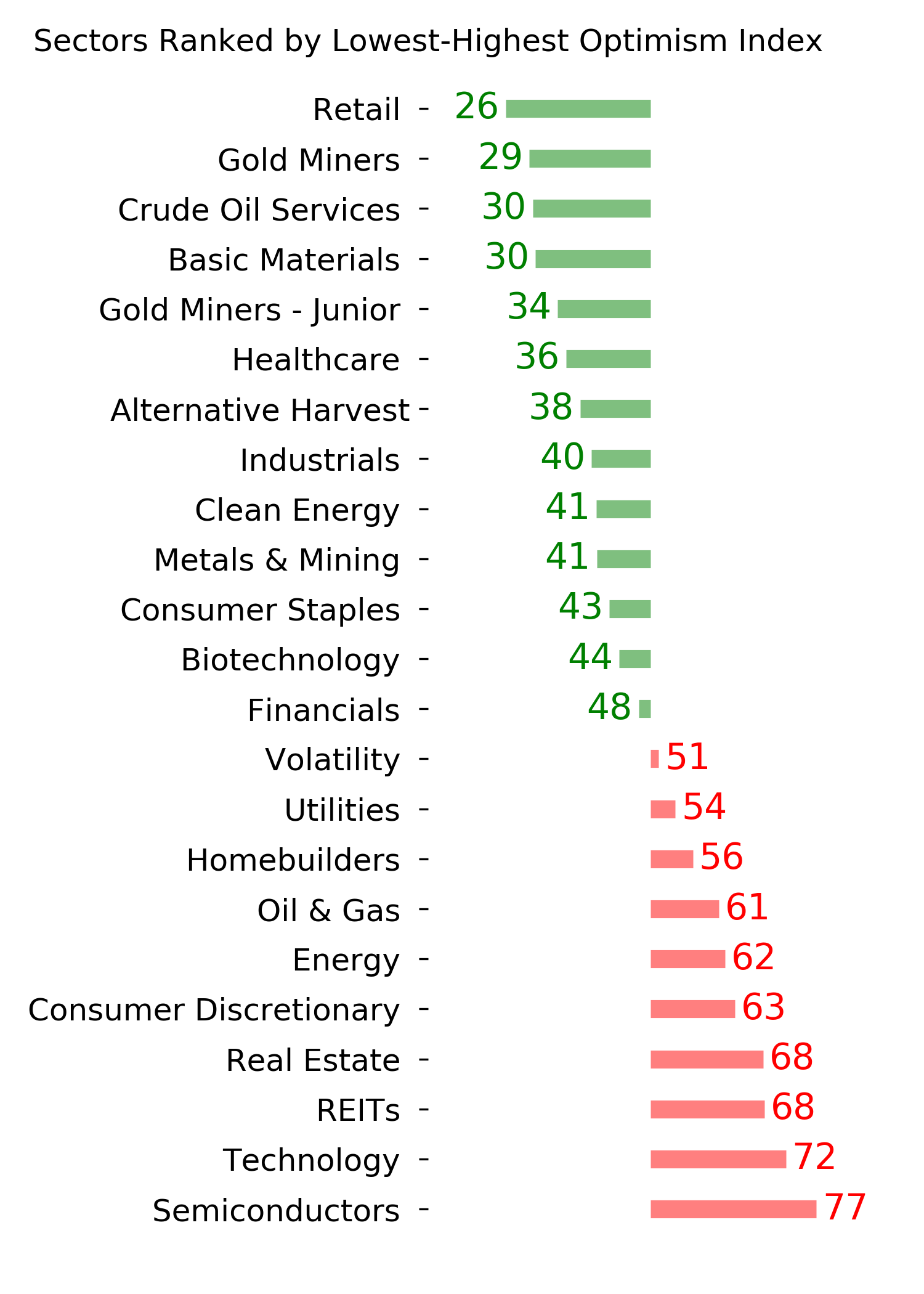

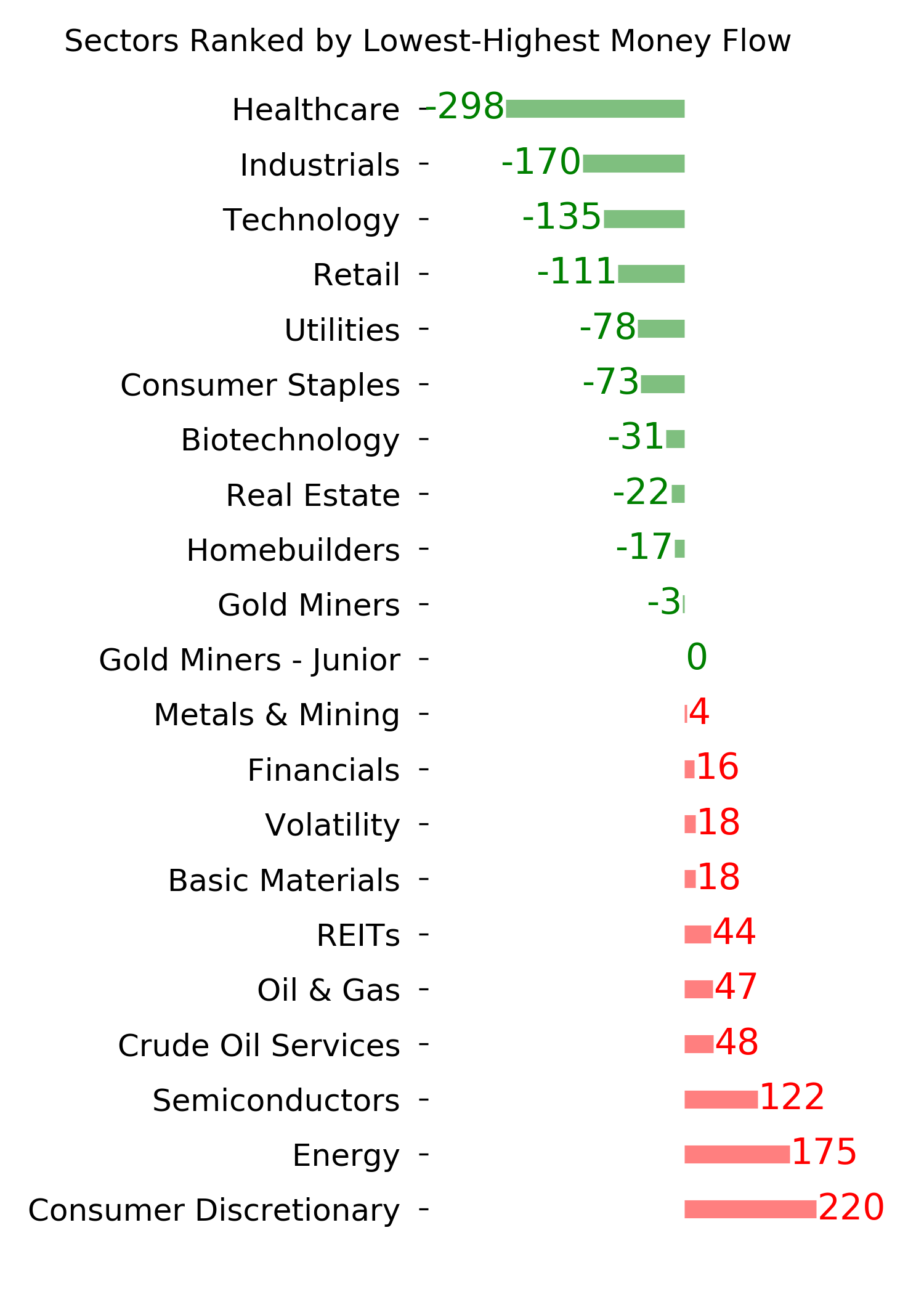

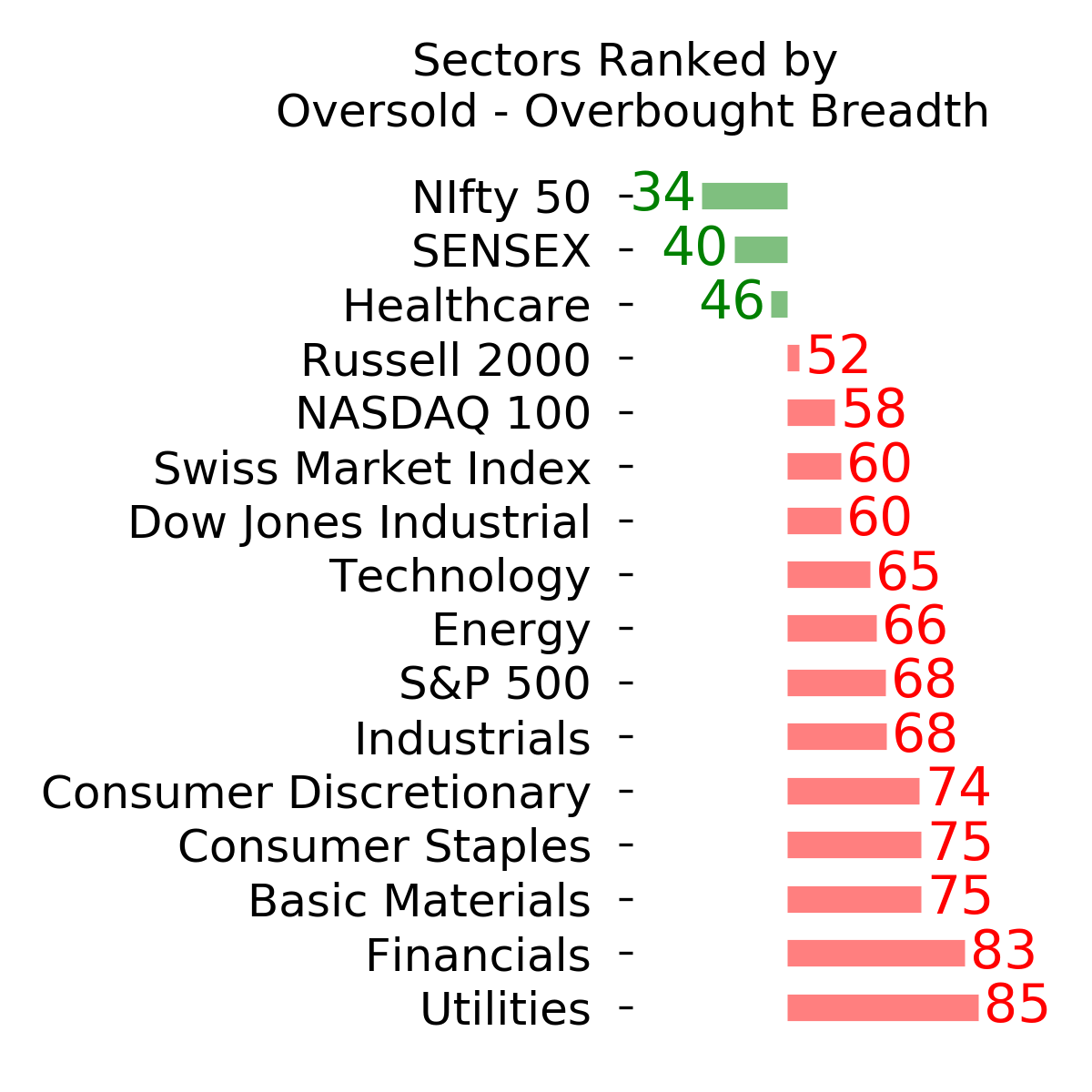

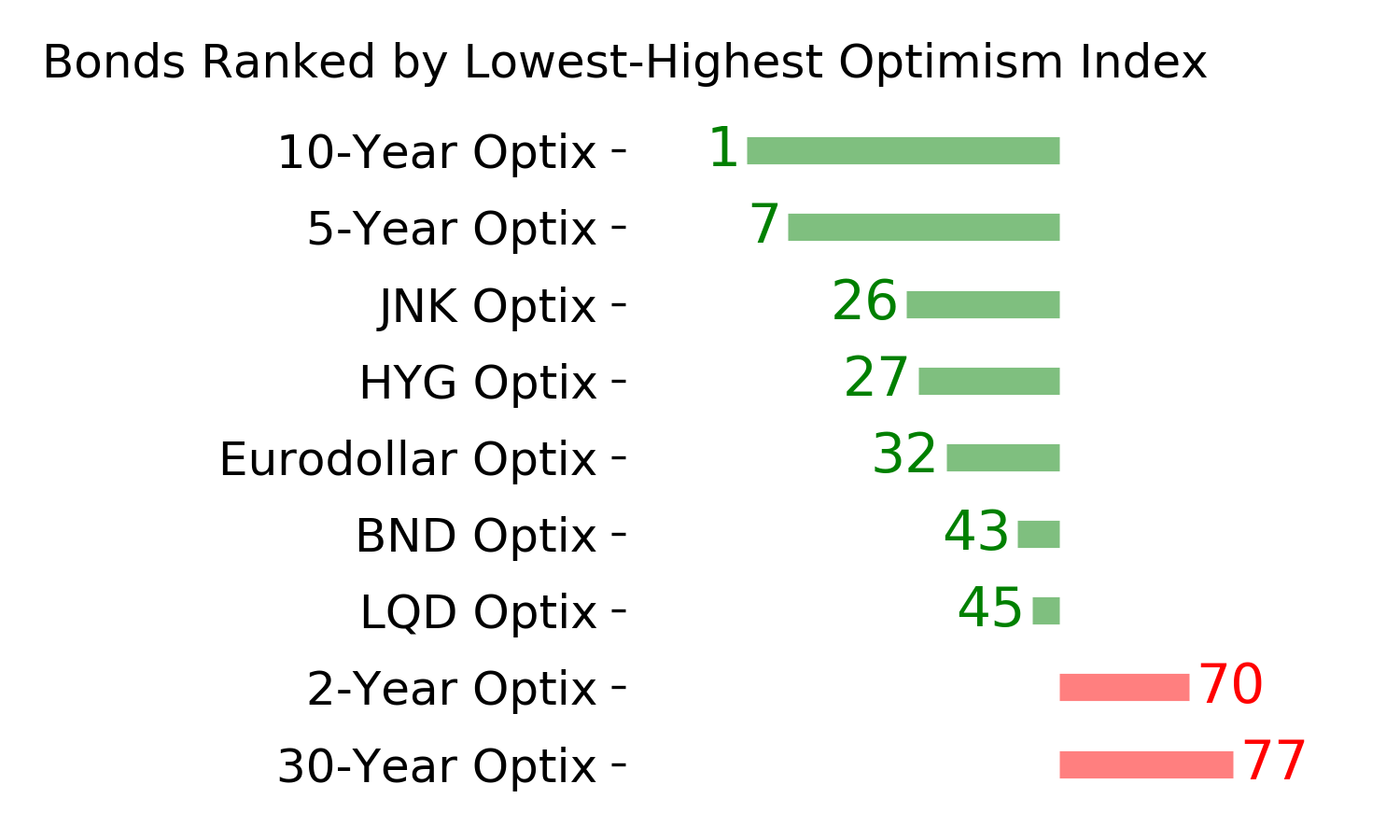

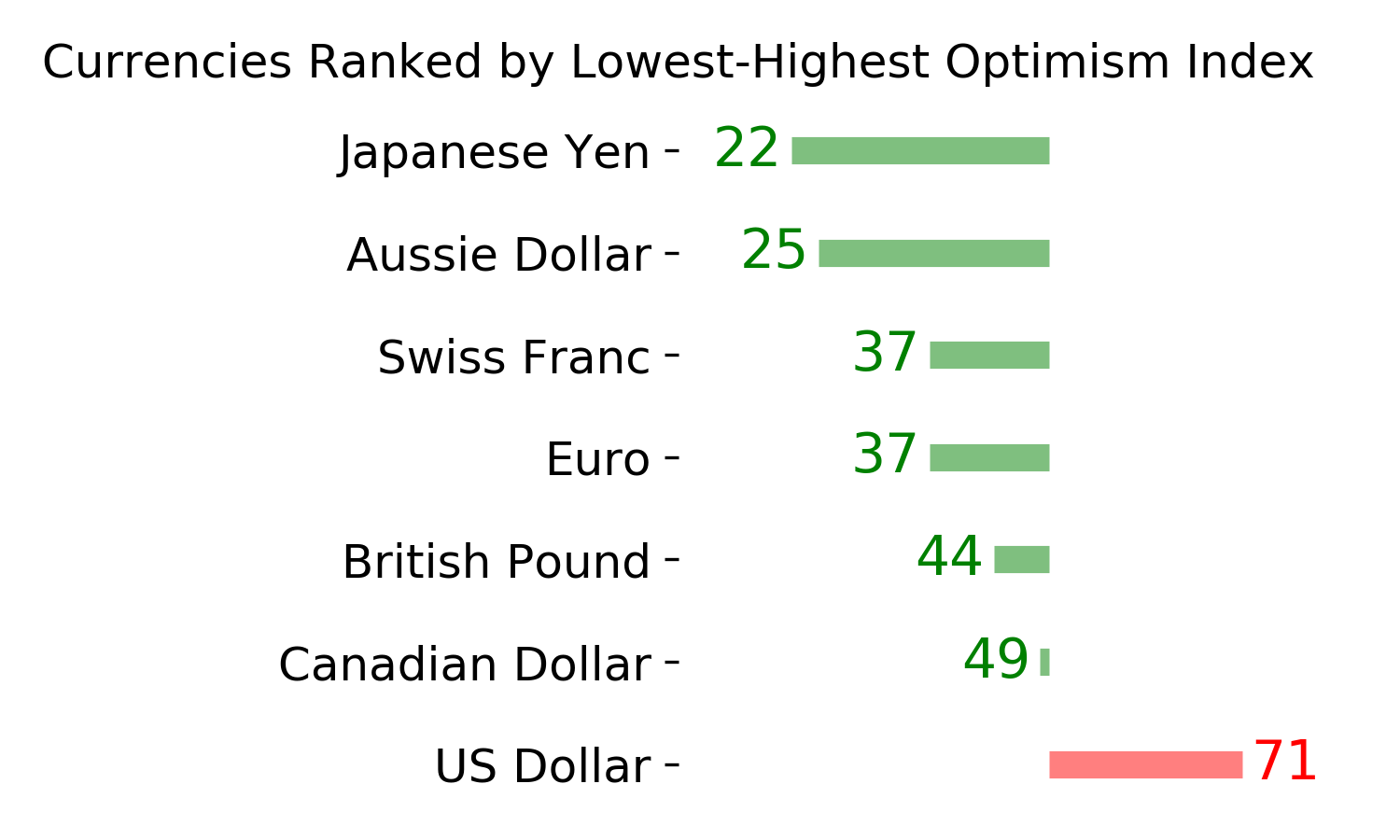

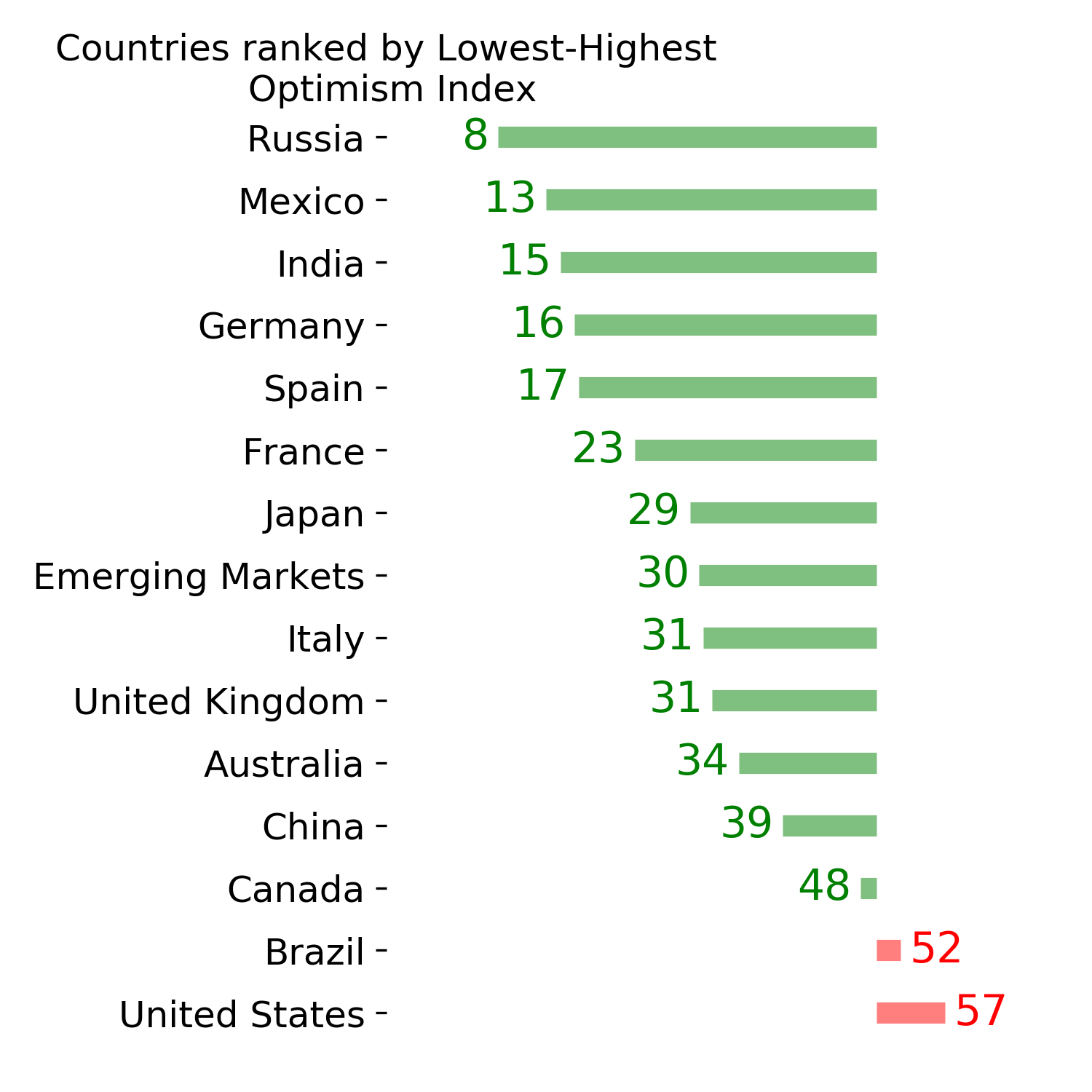

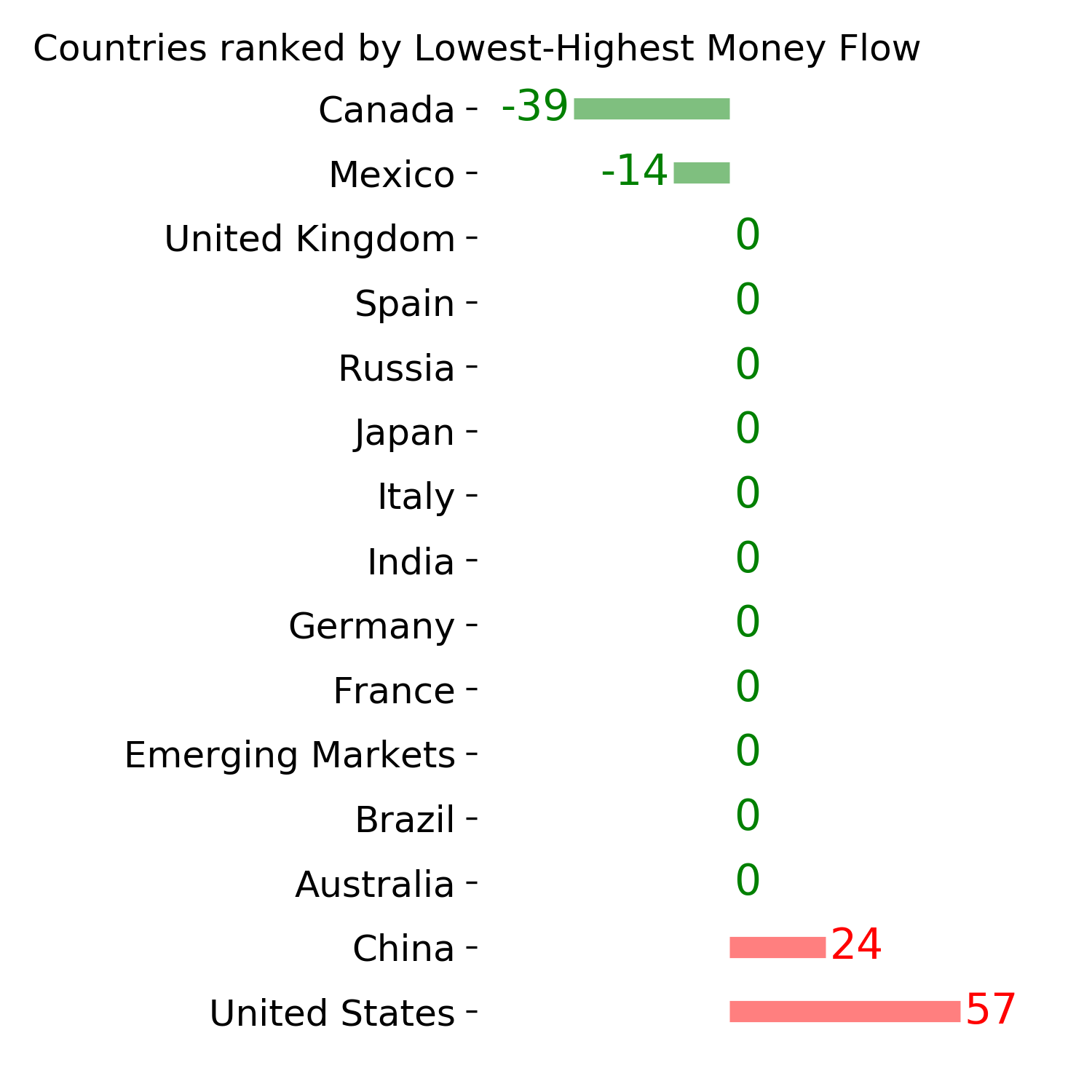

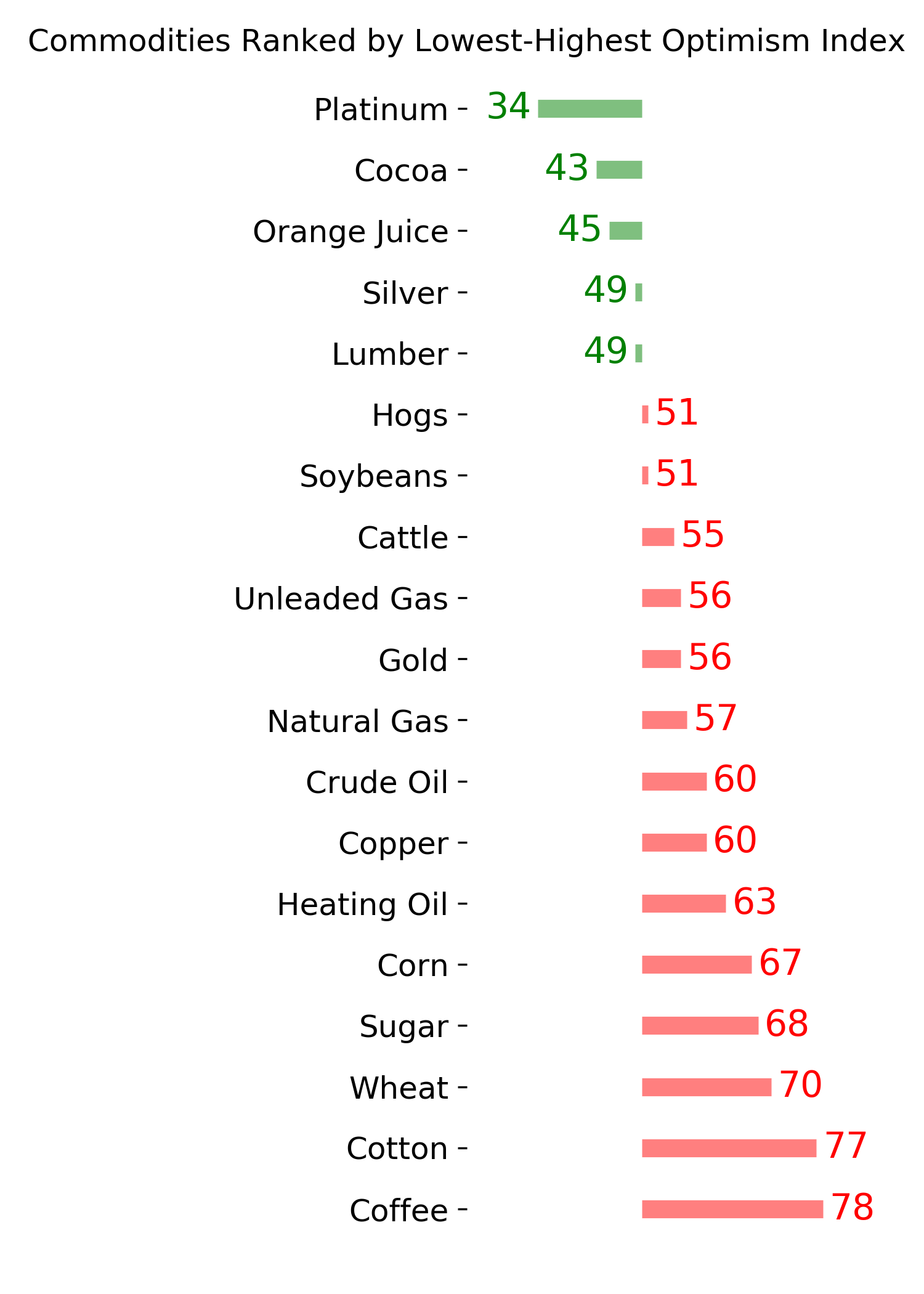

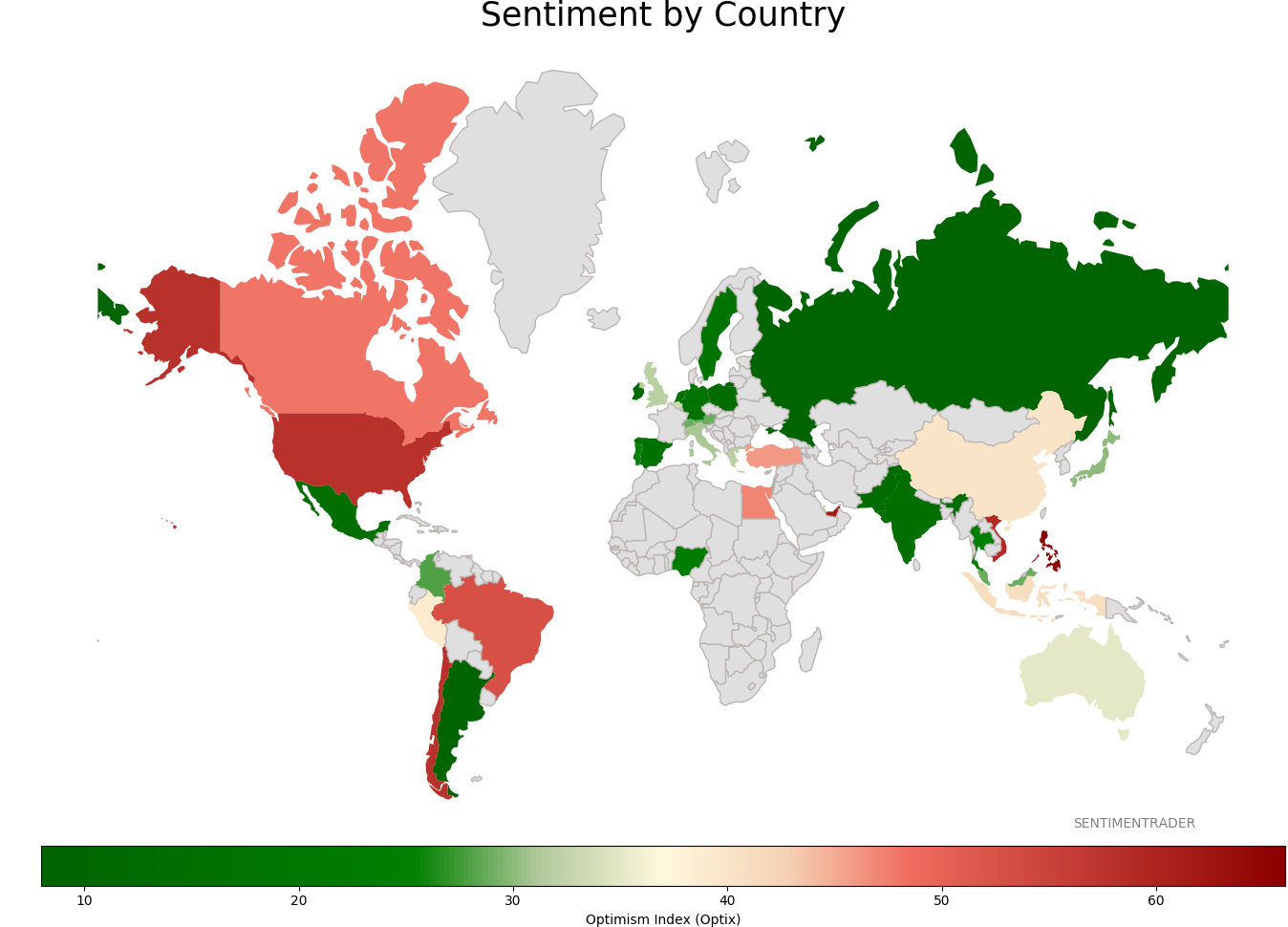

Sentiment Around The World

Optimism Index Thumbnails

|

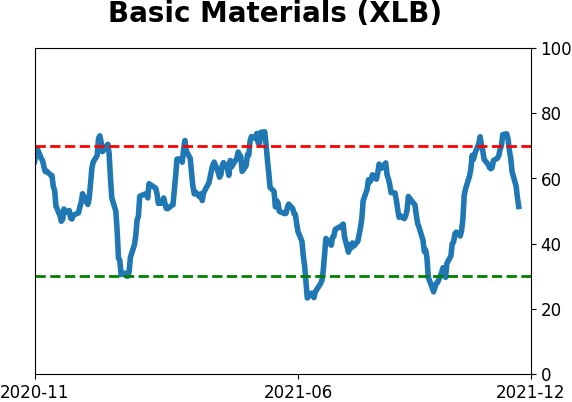

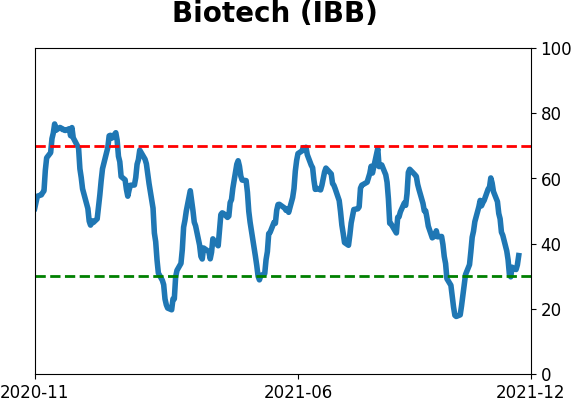

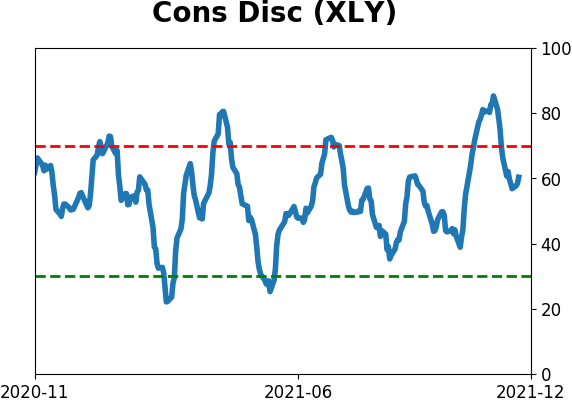

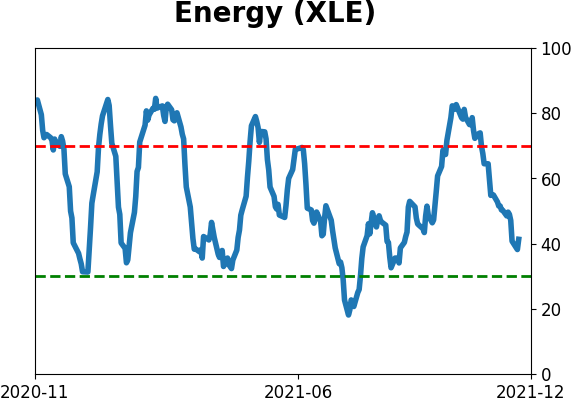

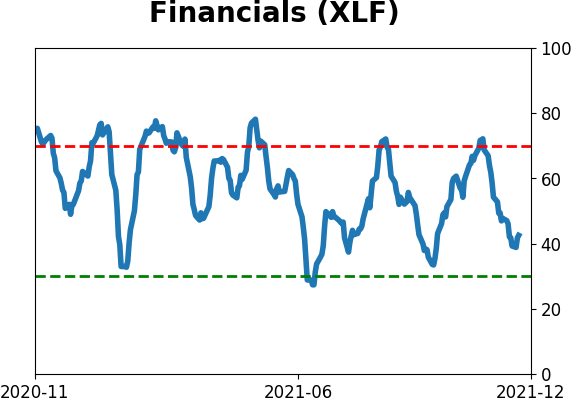

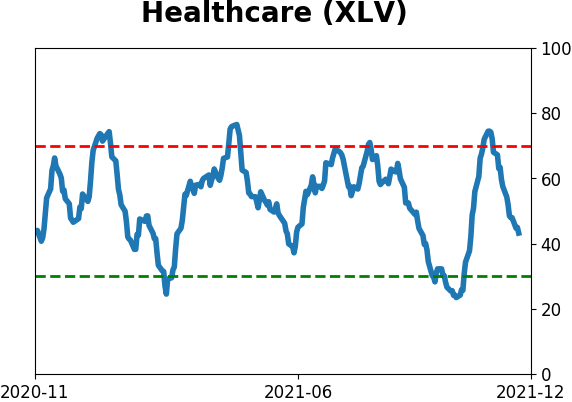

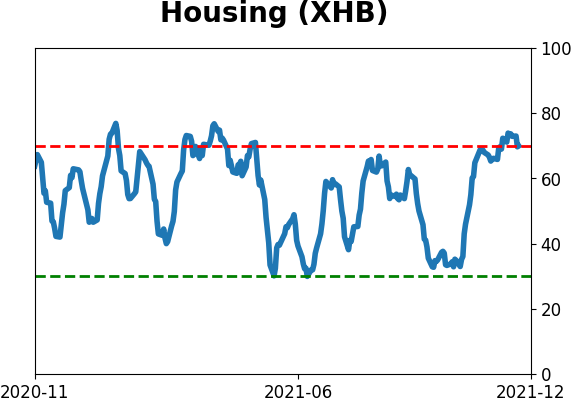

Sector ETF's - 10-Day Moving Average

|

|

|

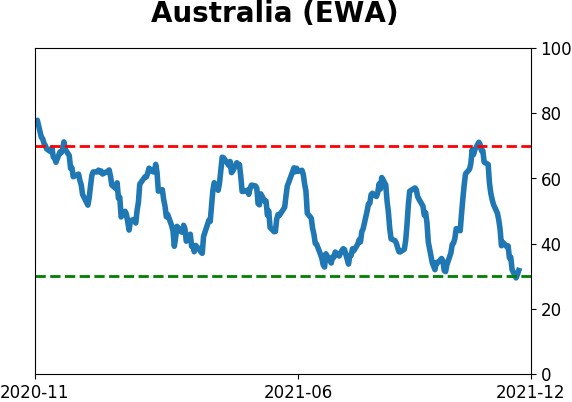

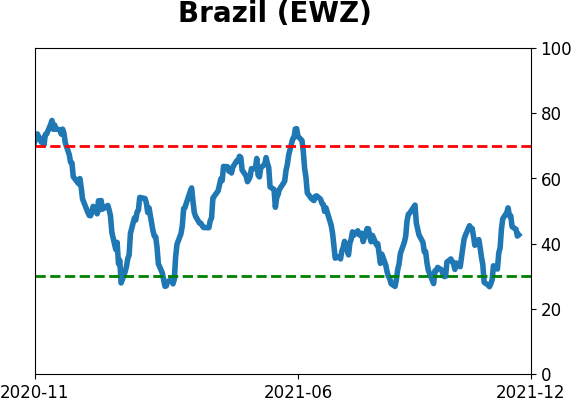

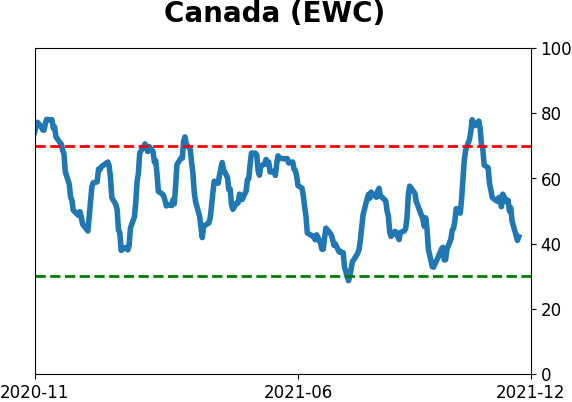

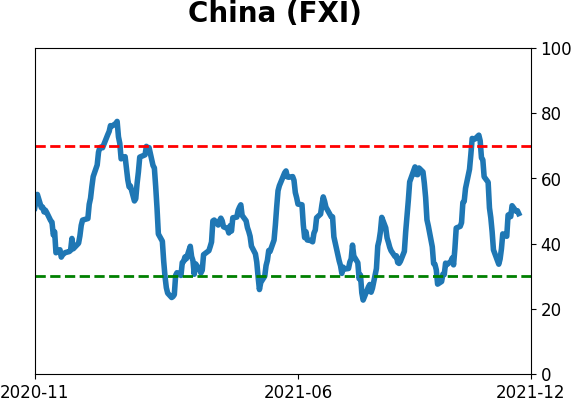

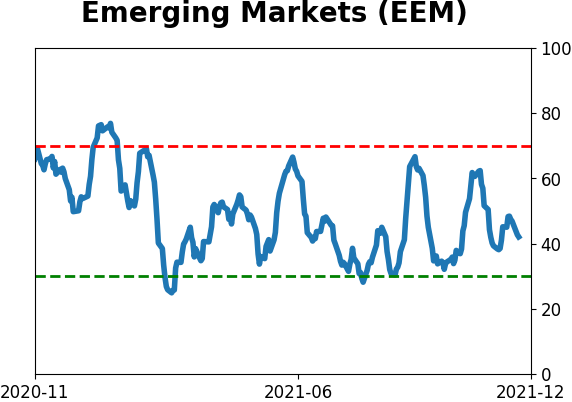

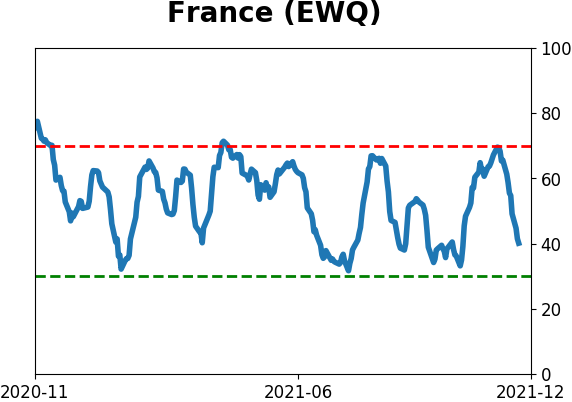

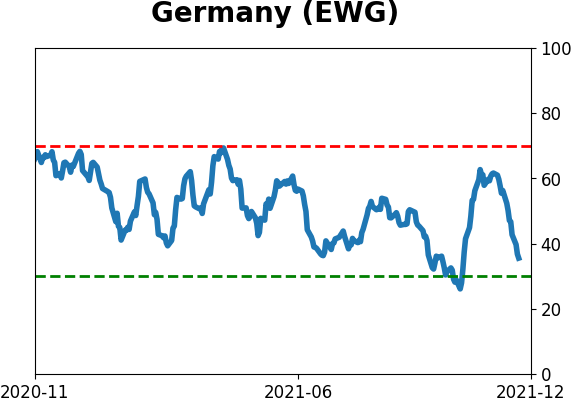

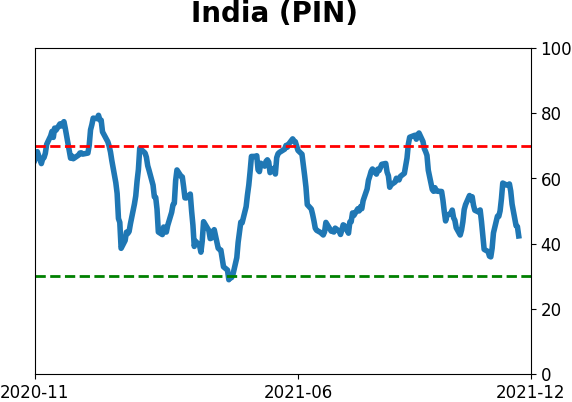

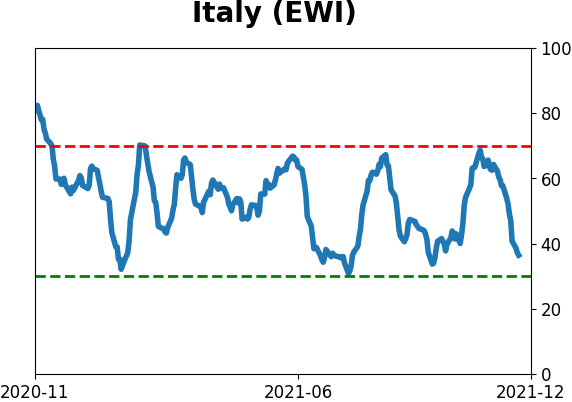

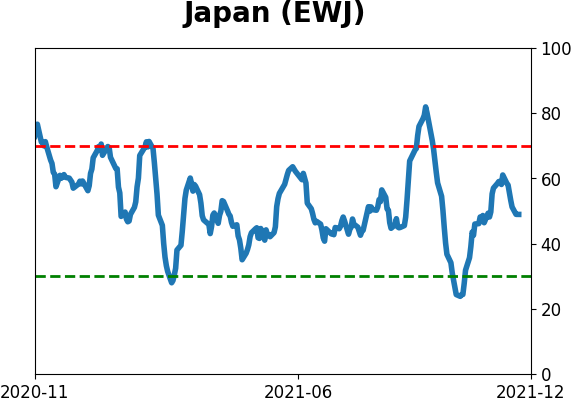

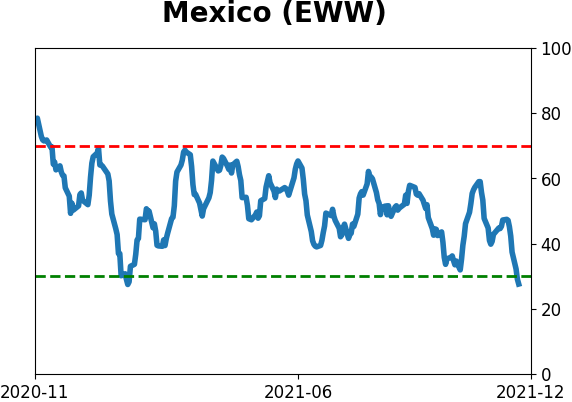

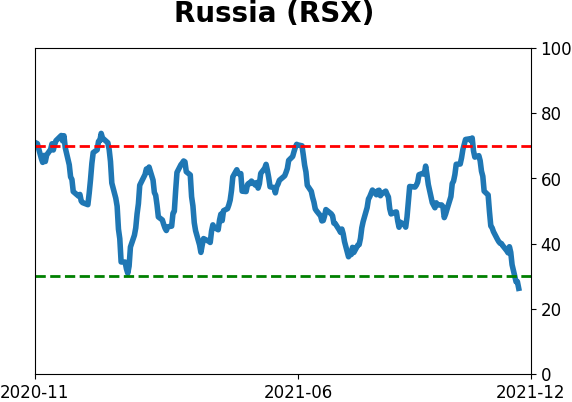

Country ETF's - 10-Day Moving Average

|

|

|

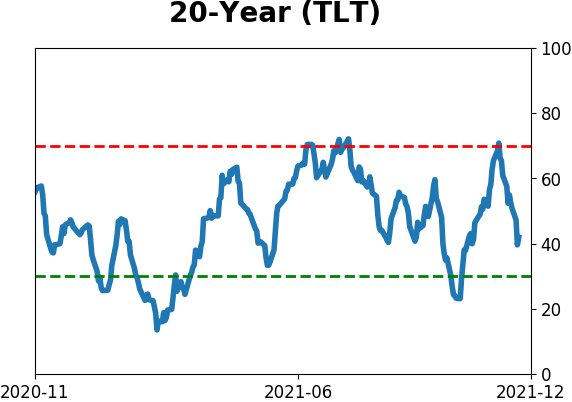

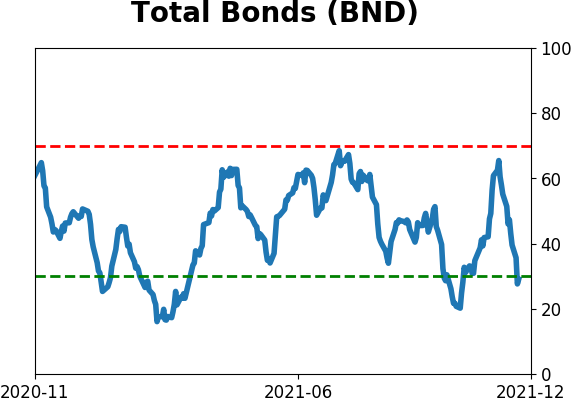

Bond ETF's - 10-Day Moving Average

|

|

|

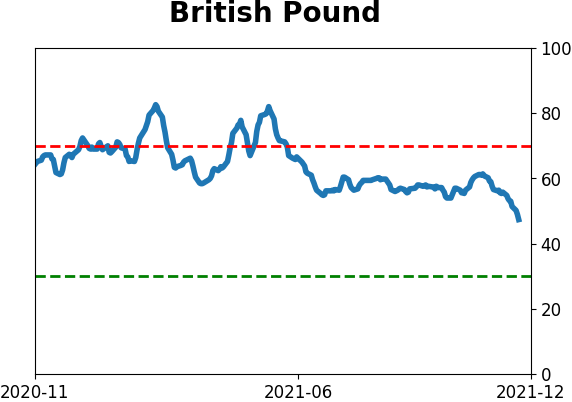

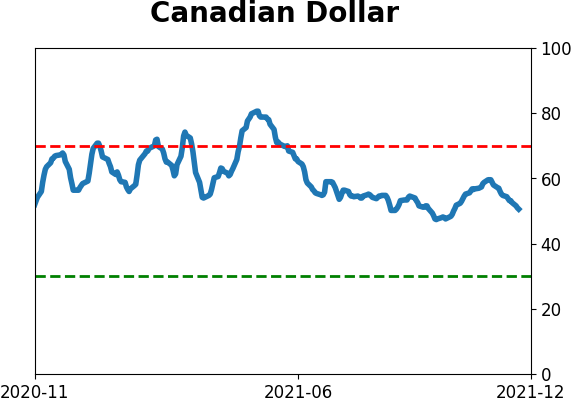

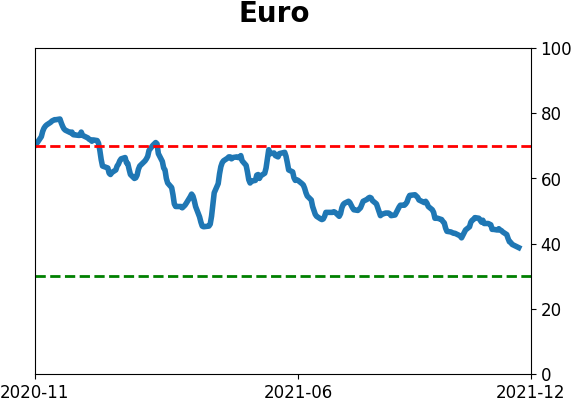

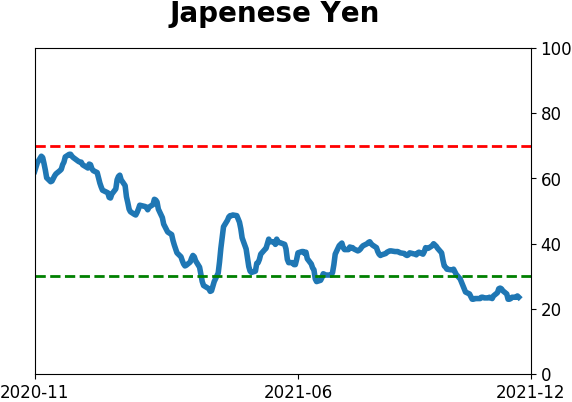

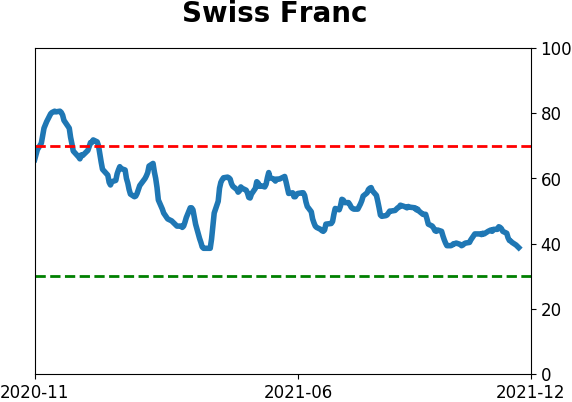

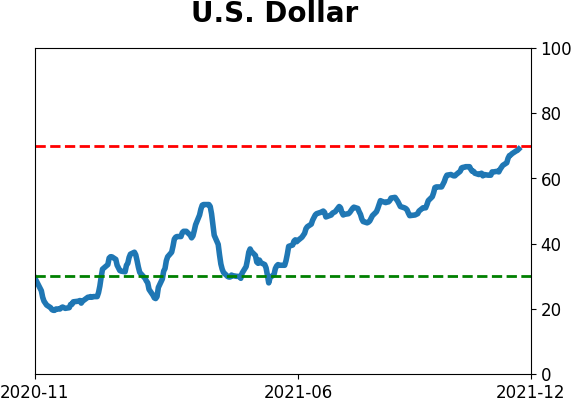

Currency ETF's - 5-Day Moving Average

|

|

|

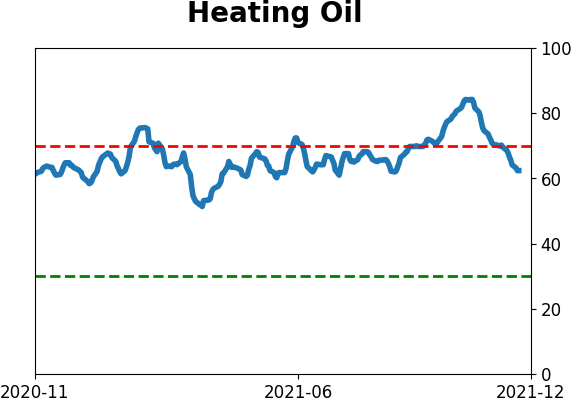

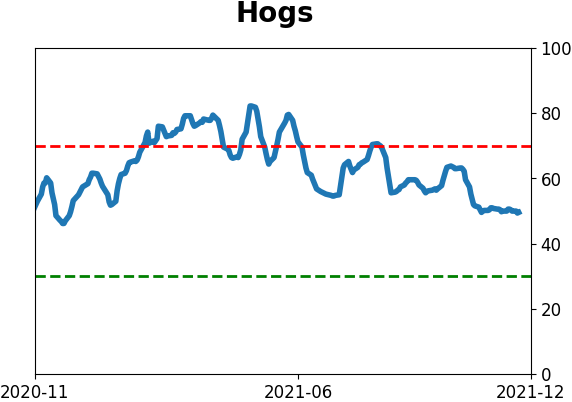

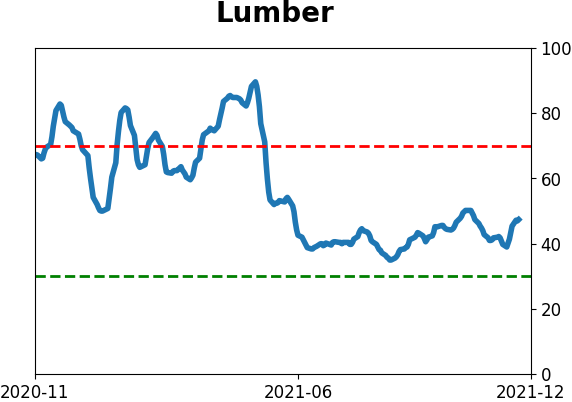

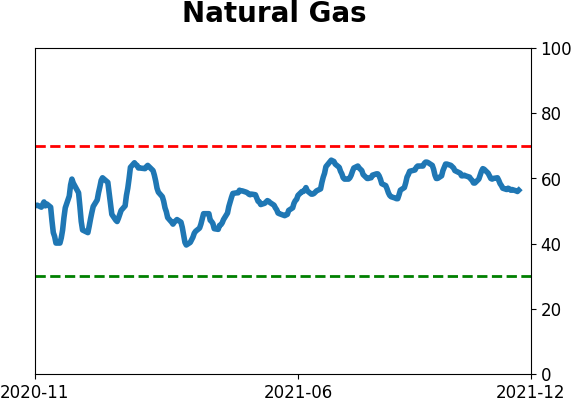

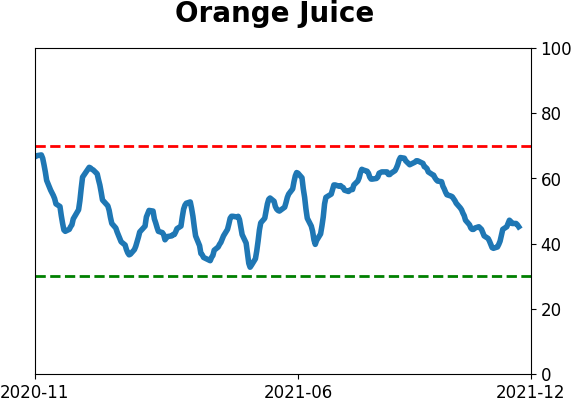

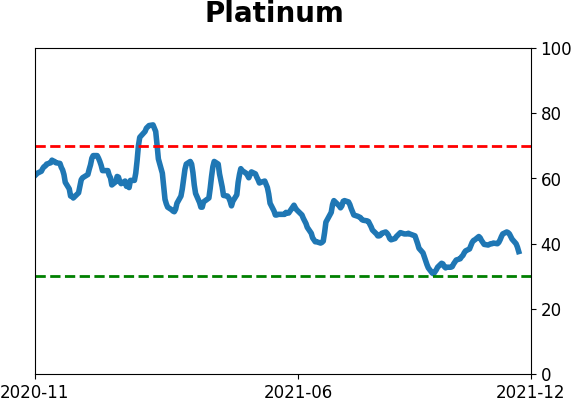

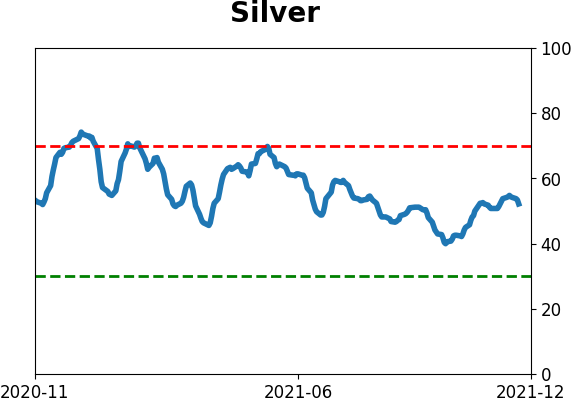

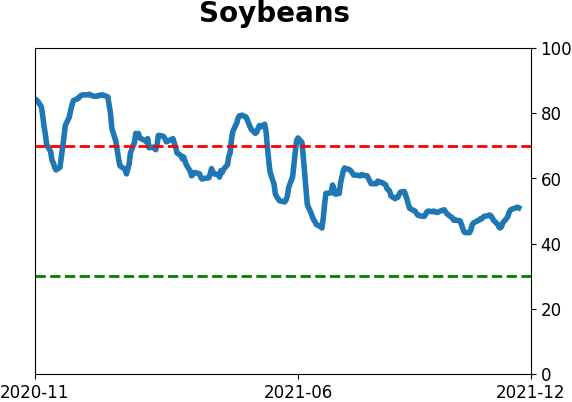

Commodity ETF's - 5-Day Moving Average

|

|