Nasdaq's Plunge

I am out of the office this week, however there have been a lot of questions about the Nasdaq's plunge on Monday. So let's look at its decline from a few different perspectives to see if Monday might be a precursor to something worse, of if there are compelling signs that it was exhaustive selling.

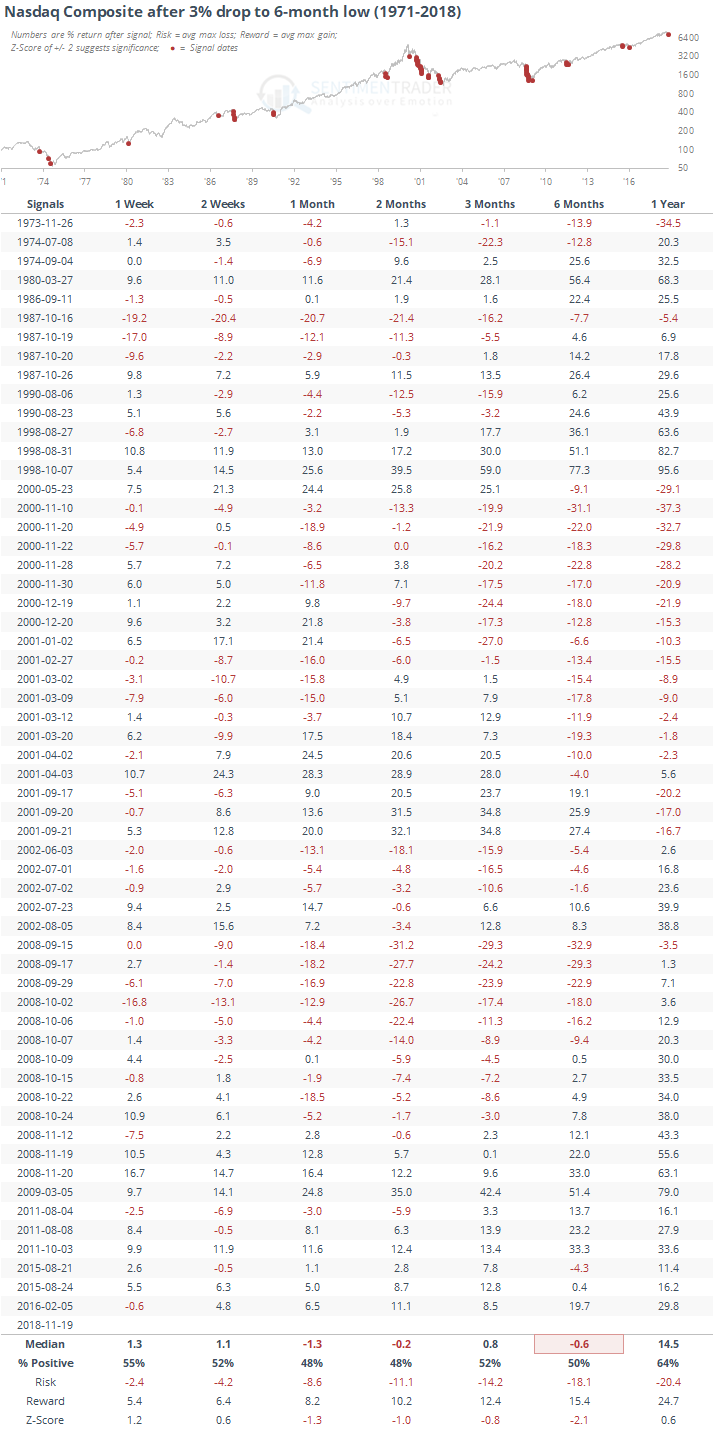

It's the first 3% decline to a 6-month low for the Composite since 2016, and every time it's happened since 2009, returns over the next 3 months were very strong, but of course we've been in a persistent bull market so that's to be expected. Overall, there were a lot of failures.

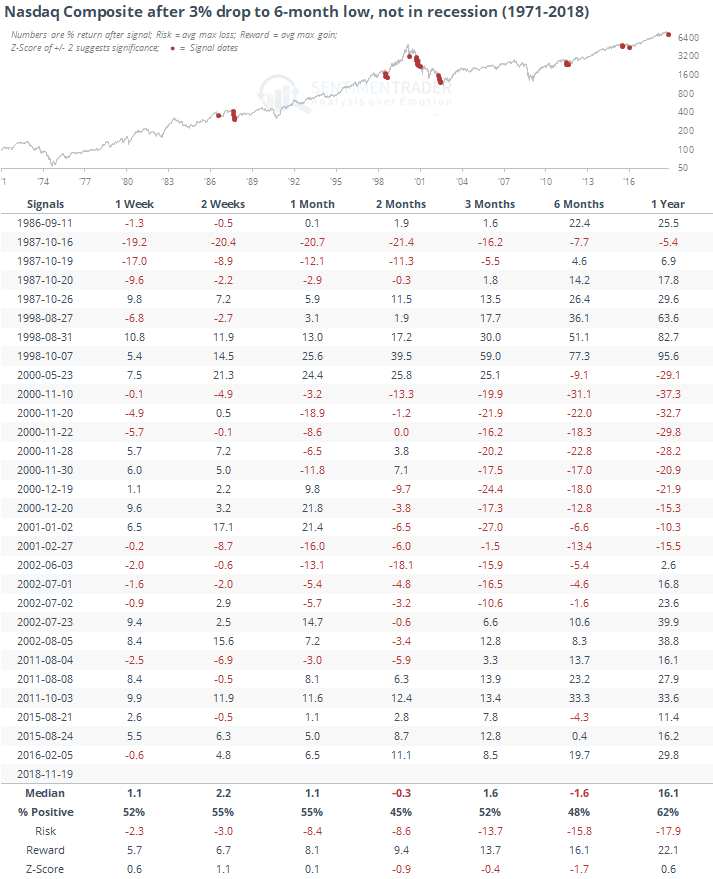

If we filter the table to only those signals when we were not currently in recession, which is essentially a 100% guarantee at the moment, then we get the following.

Still not impressive. Over the next 2 months, the Nasdaq was down more than it was up and average risk was unacceptable. But hey, it's November and we're in the most consistently positive time of the year for stocks. So how about if we look at all similar drops but only when they occur in November?

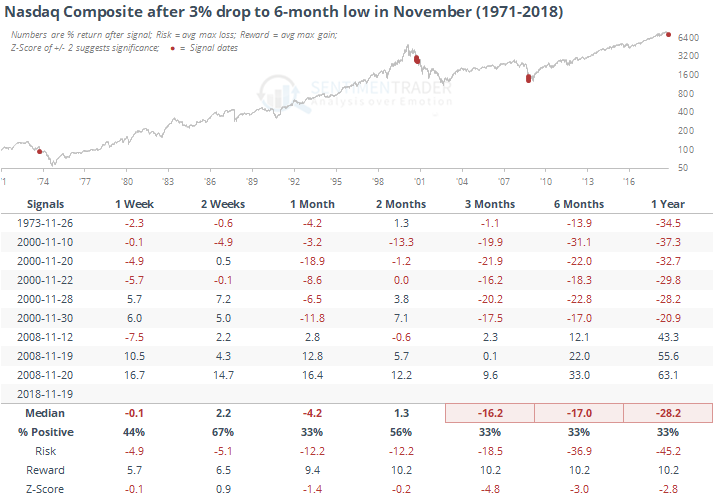

Well, that's even worse. All three times it happened (in clusters), stocks were in or heading into a bear market. When sellers didn't care about seasonality and shed tech stocks with abandon, we were heading into prolonged declines in 1974 and 2001. In 2008, at least we were in the final stages of the decline.

This is concerning.

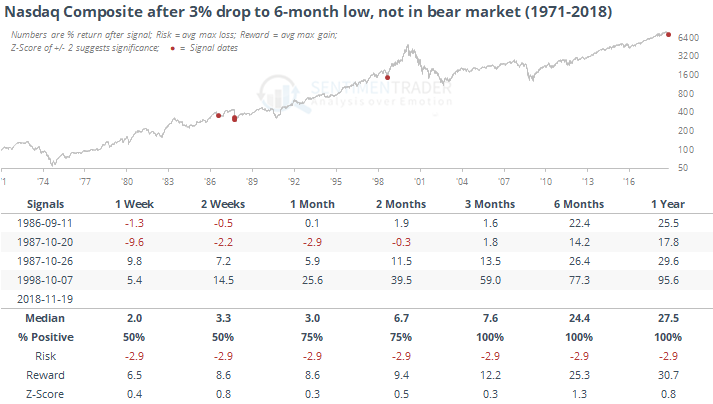

But we're not in a bear market yet. If we use the definition of bull and bear markets from Ned Davis Research, and look for big declines to a 6-month low when we're not currently in a bear market (assuming their definition is currently suggesting we're still in a bull market) then the sample size drops dramatically.

Here, there were moments of temporary panic that were, for the most part, quickly recovered. Granted, this is kind of a backward-looking filter and may not be the best way to look at it. We have to make the assumption that declines are going to stop relatively soon and/or not spread to the broader market. If that is the case, then tech stocks' returns over the next 6-12 months look fantastic. That's kind of a tautology, though.

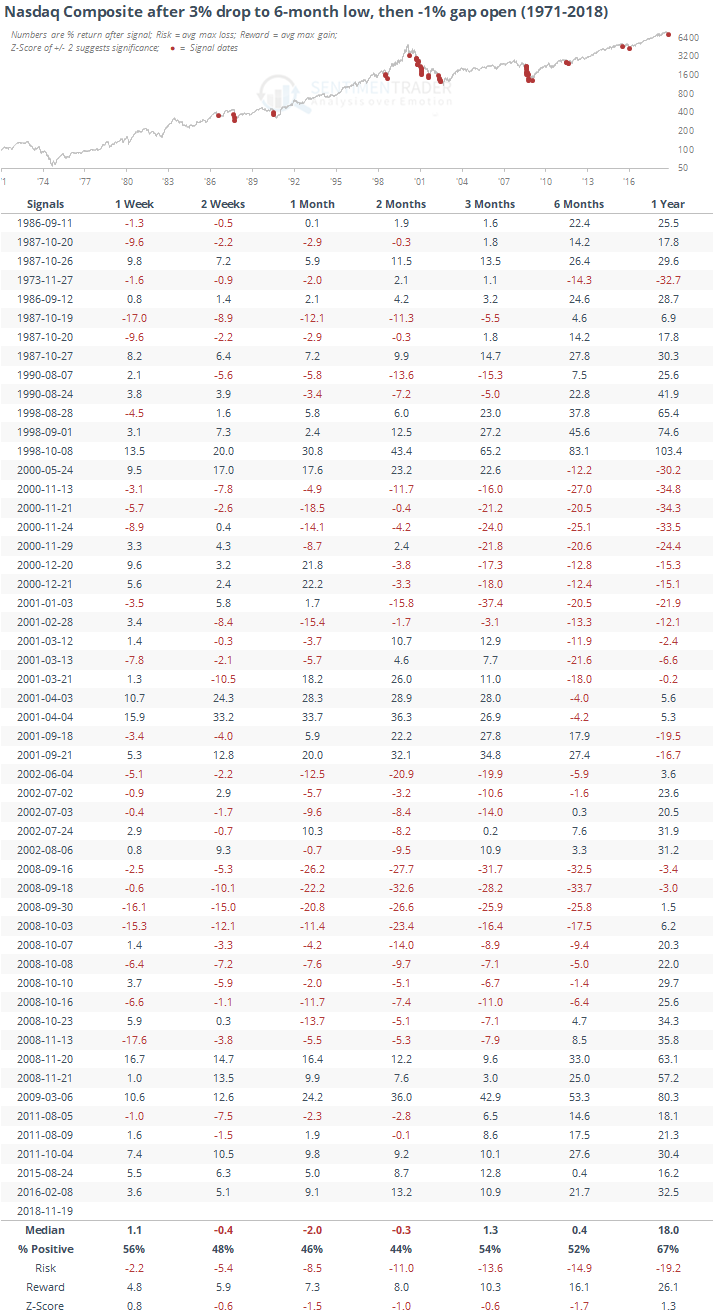

Buyers aren't showing any particular enthusiasm for tech bargains this morning, with the Nasdaq indicated to gap down another 1%. Even the usually positive pre-holiday vibes aren't working. If we look for big drops and then another big drop at the next day's open, we get this.

Still not a very good sign. In fact, it's quite bad. We usually saw further weakness in the month(s) ahead.

We didn't see a big jump in pessimism on Monday. Fewer than 40% of our indicators are showing pessimism, Dumb Money Confidence is low but not as extreme as it was in February (that's not necessarily a bad thing), and even the Short-Term Optimism Index didn't register an extreme on Monday. So other than the seasonal tendency to see a drift higher into Thanksgiving, there isn't anything among our indicators or studies strongly suggesting an imminent bounce.

We still have the very strong medium-term positive bias from everything we discussed in late October, and those had a sweet spot of 2-3 months. The volatility we've seen over the past two weeks is relatively normal after readings like that, but the new low in the Nasdaq is a definite concern. Personally, I am not reducing what is already low exposure to stocks, but I don't see anything that makes me want to increase it, either.