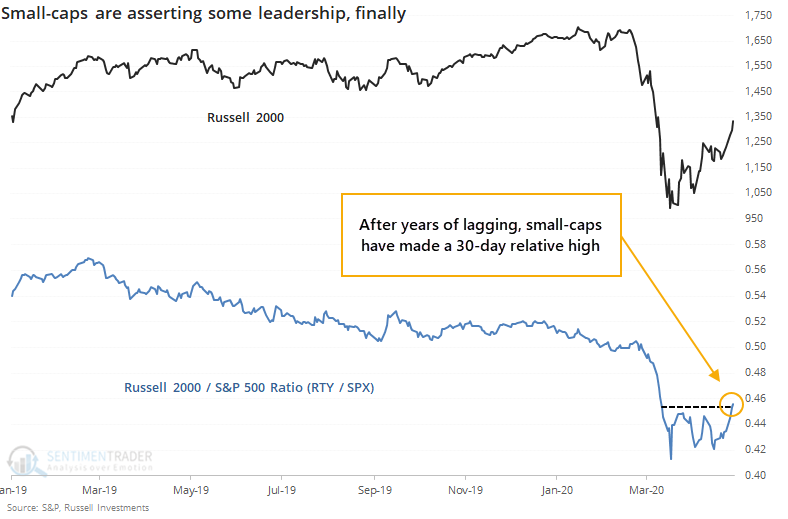

Small-cap stocks assert dominance

Try, try, and try again. After years of a relative struggle, small-cap stocks are trying to assert some dominance.

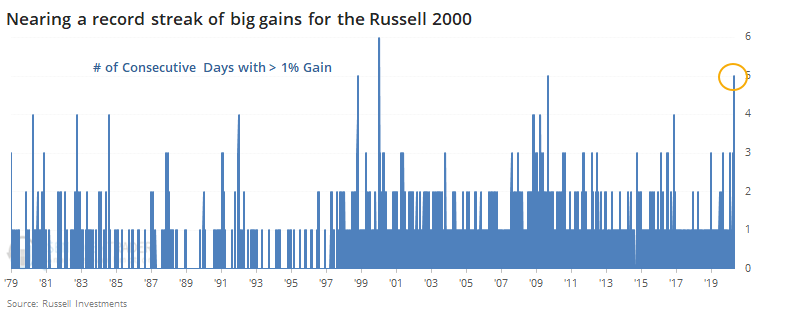

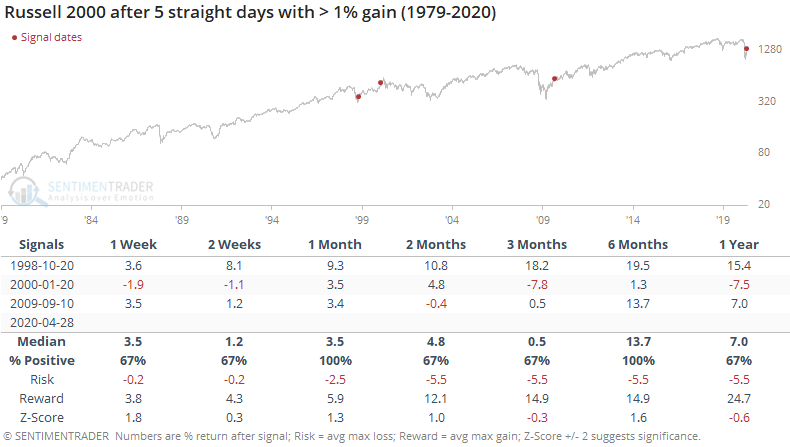

As of Tuesday, the Russell 2000 managed to gain more than 1% for five consecutive days, approaching a record streak of big daily returns.

Hitting a streak of five days of 1% gains has mostly led to gains, at least based on the 3 times it's triggered before. In 1998 it was the kick-off to even more gains in the months ahead, while the latter two see-sawed between gains and losses in the months ahead.

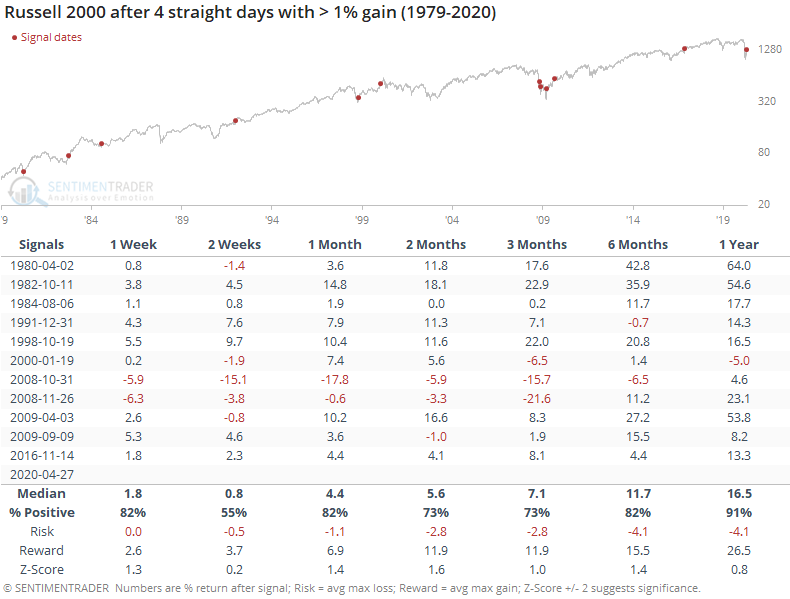

If we expand the sample size by looking for streaks of four straight days of 1% gains, then we see that returns were mostly positive, with only a single, relatively small loss over the next year.

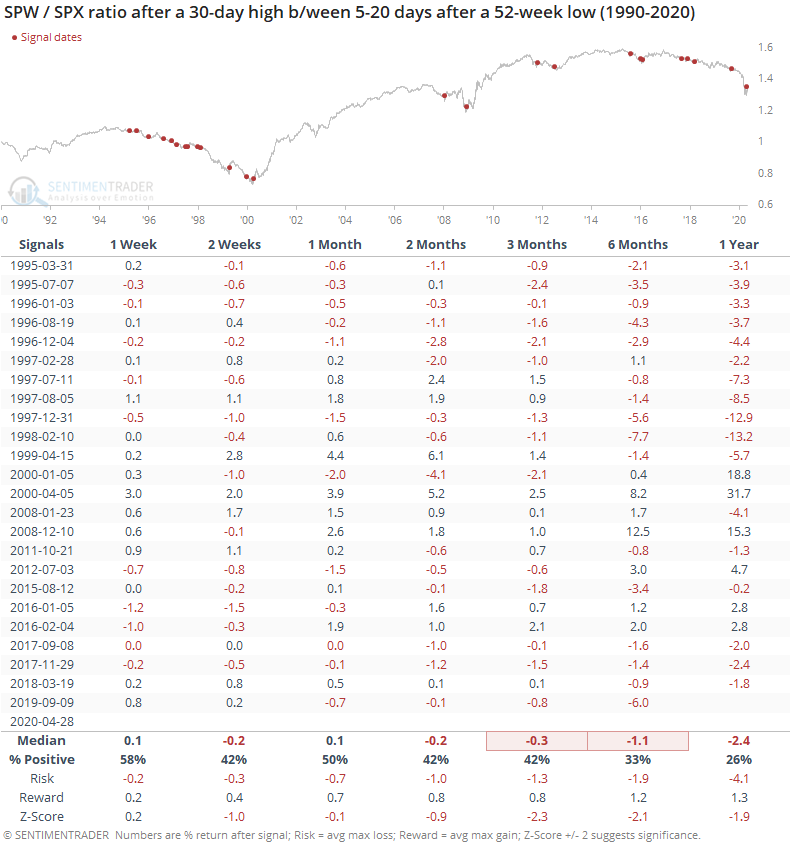

Because of this surge over the past week, the ratio of the Russell 2000 (RTY) to S&P 500 (SPX) has surged to a 30-day high, after falling to yet another multi-year low in March.

This is taken as a universally good sign, as it suggests that some of the hardest-hit companies are finding buyers. We've seen repeatedly in years past, though, that leadership in small-cap stocks is not a consistently good thing. No matter how much it might make theoretical sense, empirically the evidence is mixed at best.

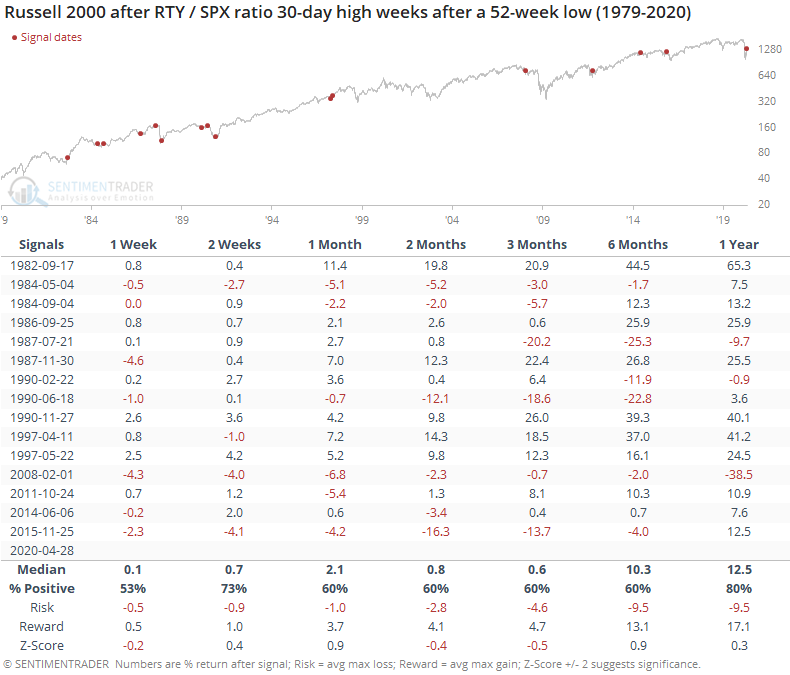

Still, let's look for times when the ratio between the Russell and S&P fell to a 52-week low, then after a period of a few weeks finally hit a 30-day high (this avoids the instances when there was a quick spike that usually failed).

For the Russell, it was an okay sign. Returns going forward were about in line with random. Over the next 2-3 months, its median return was barely positive, and by three months later, the risk/reward was about even. Not exactly awe-inspiring.

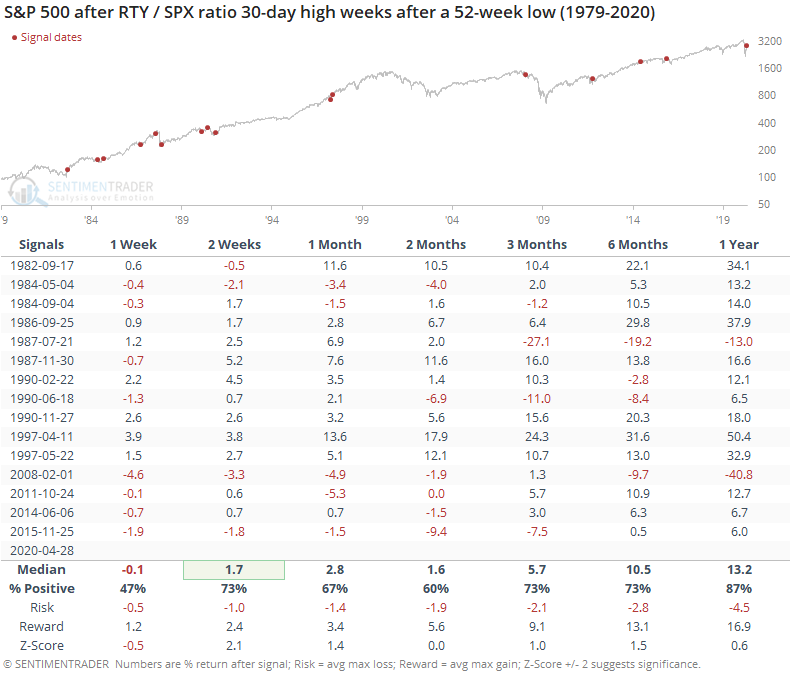

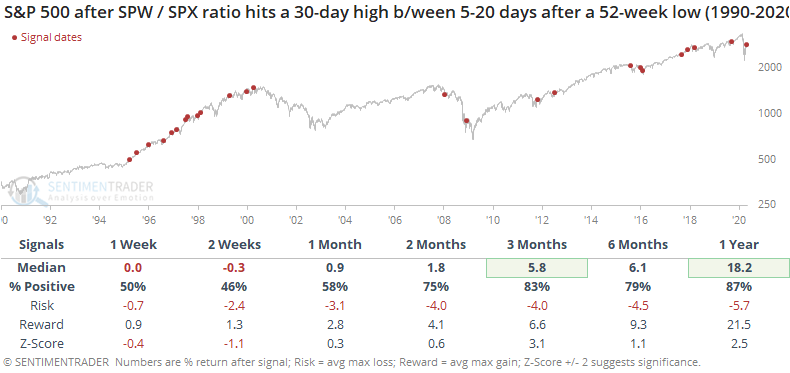

For the S&P, it was a better sign.

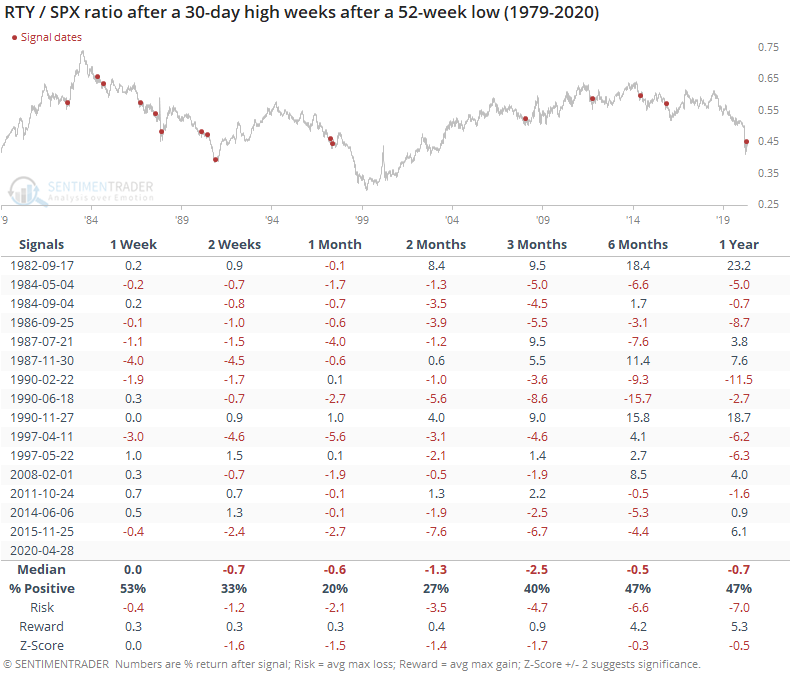

That means the ratio of the Russell to S&P usually fell.

Because of the generally negative trend in small-caps relative to large-caps in recent decades, future returns were consistently negative. Over the medium-term of 1-3 months, there was a strong bias toward the Russell under-performing the S&P after these initial recoveries.

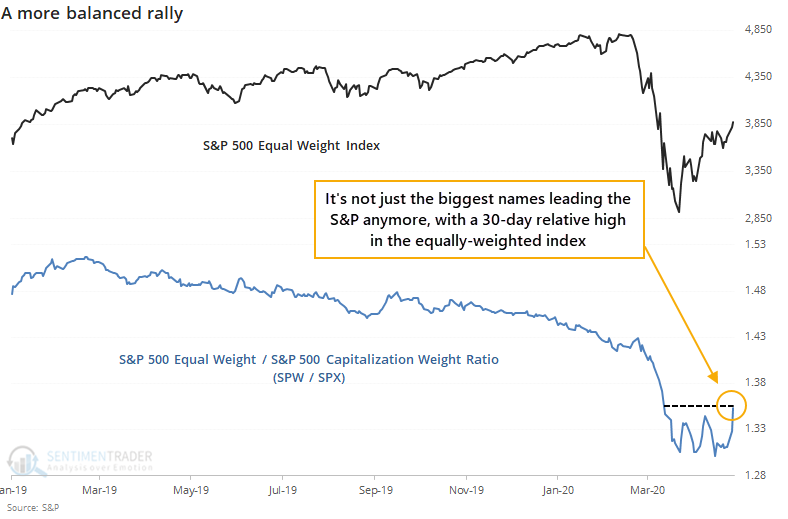

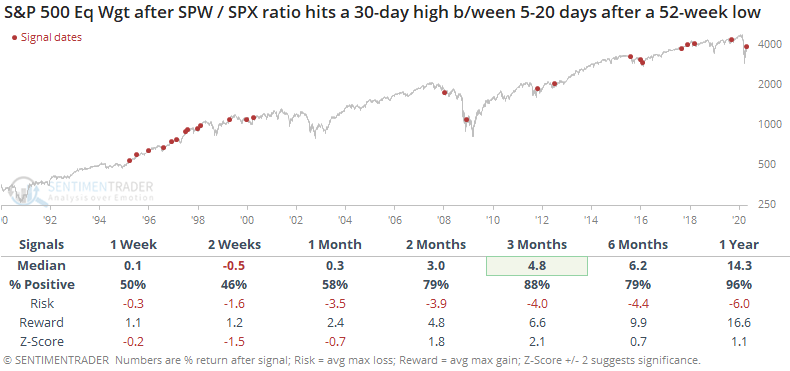

Because the rally in recent sessions hasn't necessarily been driven by the largest stocks, the equally-weighted version of the S&P 500 (SPW) has been making new 30-day highs relative to the capitalization-weighted index (SPX). This is very similar to the pattern of the Russell to the S&P.

Like we saw with the RTY / SPX ratio, this was not a consistent signal that the equal-weight S&P was going to continue to out-performed the cap-weighted index that everyone follows and benchmarks.

The cap-weighted index had a modest bias toward shorter-term weakness, but longer-term strength.

The equal-weighted index saw the same pattern, but its returns just weren't as strong.

These recoveries are mostly a good sign for the broader market. For small-caps, or even just the average stock, it's less of a good sign than it is for broader, cap-weighted indexes.