Utilities strength

NOTE: This was originally published earlier by Troy. I have added to the post at the end with the tag [Jason].

The past few days have seen U.S. stocks chop up and down. One of the few exceptions has been the utilities sector, which on a total return basis reached the highest level since the March crash:

As a result, the % of utilities stocks above their 50 dma surged from less than 15% to greater than 78% within 2 weeks. When the utilities sector rebounded this quickly in the past, it usually took a breather over the next 1-2 weeks:

The recent strength in utilities saw 3 consecutive days in which all utilities stocks were above their 10 dma:

On its own, this is a bit of a mixed signal:

But when combined with the fact that utilities are up 5 days in a row, such a strong show of momentum usually saw the utilities sector rally further over the next year:

And lastly, half of the utilities sector are above their upper Bollinger Band.

When this happened while the utilities sector rallied 5 days in a row, 3 out of 4 historical cases saw weakness over the next 1-2 weeks:

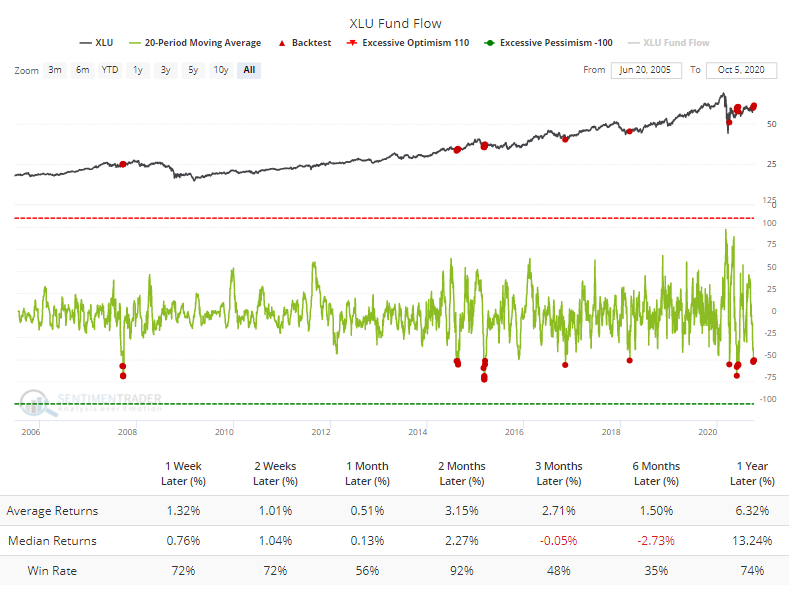

[Jason] Despite the mostly impressive performance of these stocks, ETF traders have been pulling out. The XLU fund has seen an average of more than $50 million per day leaving the fund over the past month. The Backtest Engine shows this was typically a contrary indicator, though the 3-6 month time frame was sketchy.

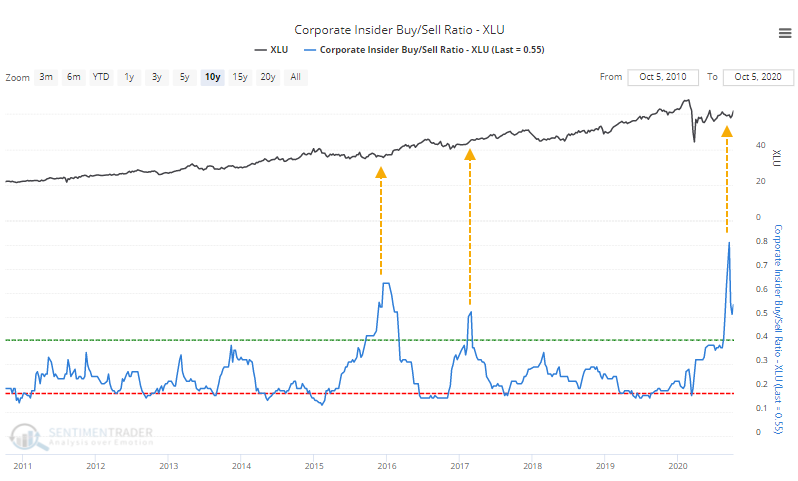

Among corporate insiders at utility companies, buying transactions have tapered off, but sales have trailed even more and have never been fewer over a 6-month time frame. That means the Buy/Sell Ratio is still historically high.

The swift decline in the ratio means that Velocity is extremely negative, but it has not been effective at preceding lower returns, unlike that measure for the broader market.

We've seen repeatedly in the past that a staid sector like utilities does not tend to do well in the short-term after big bouts of positive momentum. There are some signs of that here, and shorter-term returns have been mostly weak as noted above. Longer-term, however, the bias was solidly higher.