What You Need to Know About Inflation (Part I)

This is Part I of a short series highlighting inflation and its potential impacts on the financial markets.

The word on everyone's lips these days is "inflation" (Cue the scary music!!!). The conventional wisdom is pretty straightforward at this point in time:

- The Fed is printing money in unprecedented fashion

- Therefore, inflation is destined to soar

- All kinds of bad things will follow

- Hence all the hype regarding inflation

Did I miss anything? I don't think so. In fact, I think that sums up the current state of affairs pretty succinctly. The bottom line is that "Everybody Knows" that inflation - possibly of the significant kind - is just around the corner. Of course, there are at a minimum two potential problems here:

- Conventional wisdom doesn't always turn out to be correct (who knew?)

- Beyond all the fear and loathing what does a rise in inflation really mean for the markets?

This piece - Part I - will take a look at a simple way to analyze inflation and its potential impacts. But first a few definitions and ground rules.

What is Inflation?

A basic definition of inflation is "a general increase in prices and fall in the purchasing value of money." Over time, prices typically rise. As long as that rise is slow and steady, no problem. The potential problems occur when either:

- Inflation reaches a level where prices are rising very quickly (and outstrip wage growth in the process)

- Inflation actually goes negative - which is referred to as deflation

Most people - OK, many people - budget. As succinctly as possible, they figure out their take home pay, total up their expenses and try to make sure the former is greater than the latter. However, if inflation reaches a certain level and their expenses begin to rise much more quickly than they planned for, well, if you never understood the danger of high inflation - now you do. And the higher the rate of inflation, the greater and more quickly the trouble grows.

Interestingly, deflation - a trend of lower prices - if persistent, is actually a worse situation. As prices fall buyers begin to put off buying goods and services with the expectation of "buying cheaper" down the road. As more and more buyers stop buying, fewer goods and services are produced and sold. Eventually companies start making less and contracting their operations in the face of declining demand. And so on and so forth in an ever-shrinking process until the whole thing just kind of collapses in on itself (if you never understood the Great Depression of the 1930's - now you do).

So, the ideal is a relatively low, steady rate of inflation. Does this really matter? Consider that since the double-digit inflation era of the late 1970's and early 1980's we have been in a "disinflationary" environment. During that time, we have seen the stock market post it's greatest 40 years in history AND the bond market has (at least until recently) been in a roughly 40-year bull market, with rates falling from roughly 15% to roughly 1% (more on all this in a moment).

Hence the fear and loathing that an outbreak of inflation might "upset the apple cart."

How Do We Measure Inflation?

For better or worse, the standard measure of inflation is the 12-month rate-of-change in the Consumer Price Index (CPI). According to Investopedia.com, "The Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care. It is calculated by taking price changes for each item in the predetermined basket of goods and averaging them. Changes in the CPI are used to assess price changes associated with the cost of living. The CPI is one of the most frequently used statistics for identifying periods of inflation or deflation."

Now lots of people like to quibble with how the CPI is calculated and what's included and what's not. For example, some will strip out energy and/or transportation and insist that everyone focus on what they refer to as "core inflation." Fine. More recently some have accurately noted that the way housing costs are calculated within the CPI was changed and - in their opinion - no longer accurately portrays housing costs for much of the population. And maybe they're right. But here at www.Sentimentrader.com Jason is pretty adamant that we "stick to the facts" (and thank goodness not the darker places that my market-addled mind sometimes wanders).

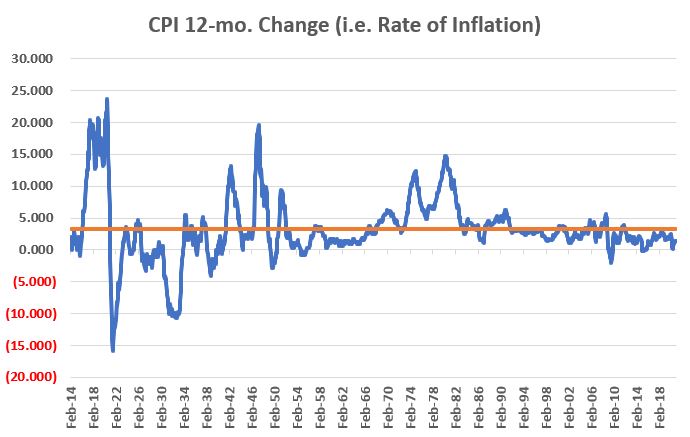

So here are some facts. In the chart below:

- The blue line displays the 12-month change (i.e., the rate of inflation) in the CPI since 1914

- The orange horizontal line represents the long-term average of 3.22%

Things to note:

- The big fear is the significant loss of purchasing power that results when inflation reaches a very high level that persists for any length of time

- There have been 5 bouts of major inflation, where the rate of inflation exceeded 10%:

- 1916-1920

- 1941-1943

- 1946-1948

- 1974-1976

- 1978-1982

- Since the early 1990's, inflation has rarely poked its head about the long-term average of 3.22%

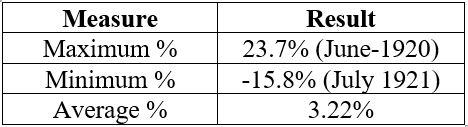

Has this long period of "disinflation" helped investors? The chart below displays the rolling 40-year return for the Dow Jones Industrial Average. As you can see, the last 40 years has been by far the best ever for stock investors (as an aside, this is a fact we should celebrate and be grateful for, but not a fact that we should fall in love with or expect to continue ad infinitum into the future. But that's a topic for another day).

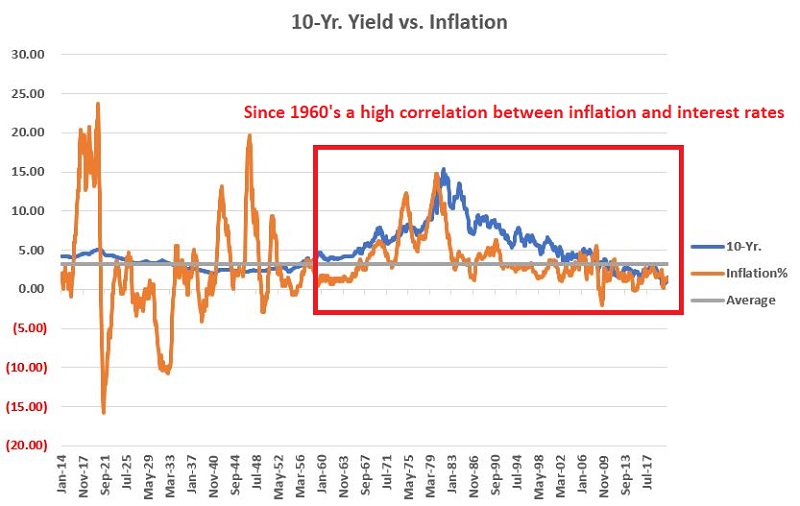

In the chart below:

- The blue line shows the yield on 10-yr. treasury notes

- The orange line shows the CPI 12-month rate of inflation

- The grey line shows the long-term average rate of inflation

More things to note:

- Since January 1960 the correlation coefficient between 10-year yield and CPI 12-month change has been quite high at 0.69 (1.00 means they move exactly the same)

- Generally speaking, interest rates (i.e., yields) fall when inflation is below its long-term average and rise when inflation is above its long-term moving average

- As you can also see, the long period of disinflation we have enjoyed in recent decades has helped to push interest rates to their lowest levels ever

- If you did not understand why so many people are concerned about a reversal of inflation upsetting the "Goldilocks" environment we have enjoyed for stocks and bonds for the past several decades - now you do.

In Part II we will get more into the details of market performance during different types on inflationary environments.

Until then, try to remain calm...